The Rocket, The Bubble, and The Metal Nobody Wants to Talk About

On a humid evening in South Texas, thousands of people stood watching a stainless-steel rocket tower over the launch pad like something pulled from a science-fiction novel. Cameras pointed skyward. Livestreams counted down. Engineers, investors and enthusiasts waited for another attempt to push humanity closer to Mars.

When SpaceX launches, it feels as though the future briefly arrives ahead of schedule.

That sensation matters more than most people realise.

Markets have always gravitated towards stories that promise a break from historical constraints. Railways did it in the nineteenth century. Radio did it during the roaring twenties. The internet did it in the late 1990s. Today, artificial intelligence and private space exploration occupy much the same territory in the public imagination. They suggest that old limitations no longer apply and that extraordinary gains sit just beyond the horizon.

SpaceX has earned much of the admiration directed towards it. Rockets land themselves. Launch costs have collapsed. A private company has achieved things that many national governments struggled to deliver despite vastly larger budgets. There is nothing speculative about those accomplishments.

Yet that is precisely what makes SpaceX so interesting.

Every market cycle eventually finds an asset, a company or an idea that becomes larger than itself. It stops being valued purely on revenue, earnings or cash flow. Instead, it becomes a vessel for collective optimism. Investors begin projecting onto it everything they hope the future will look like.

SpaceX increasingly feels like that company.

Not because the technology is fake.

Because the technology is real.

The railway boom had railways. The internet boom had the internet. The great speculative episodes in financial history rarely emerge from fraud. They emerge when genuine breakthroughs convince investors that traditional valuation disciplines no longer apply.

Early in a bull market, few people care.

It begins to matter enormously near the end.

When Money Becomes Easier Than Value

The fascination with SpaceX reveals something larger than the company itself.

It reveals the environment that produced it.

For much of the past decade, investors have been conditioned to view almost every setback as temporary. Corrections became buying opportunities. Higher valuations became evidence of superior business quality. Concerns about price were often dismissed as proof that critics simply failed to appreciate technological change.

Since the Global Financial Crisis, and particularly since 2020, the amount of money circulating through the financial system has grown at a pace rarely witnessed in modern history.

That liquidity had to go somewhere.

It found its way into property, bonds, private markets, cryptocurrencies and, above all, equities.

This is often forgotten during periods of market euphoria. Investors tend to attribute rising asset prices entirely to innovation, productivity or superior corporate performance. Yet the backdrop matters. A great deal of wealth has been created over the past fifteen years. A great deal of money has also been created.

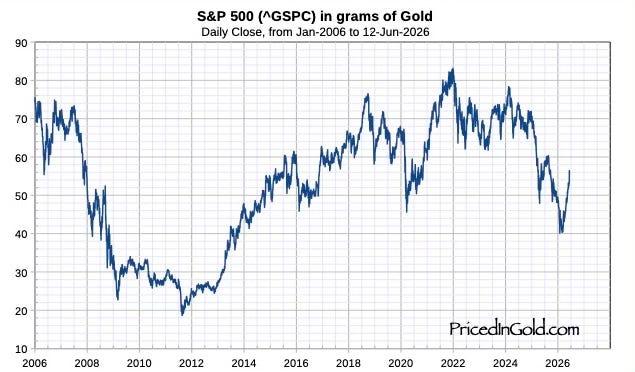

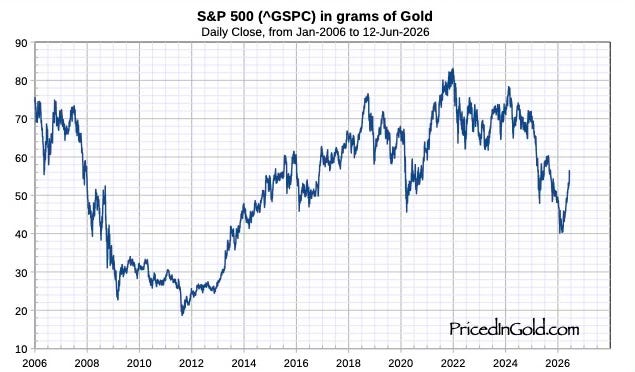

When equities are measured against gold instead of paper currency, the picture starts to look rather different.

The chart paints a less flattering picture.

Many of the spectacular gains celebrated over recent years appear considerably less spectacular when measured against an asset whose supply cannot be expanded by policymakers or commercial banks. The rise remains visible, but the magnitude changes. So does the interpretation.

The Long Shadow of Liquidity

Liquidity, more than technology, has been the force shaping modern markets.

Following the financial crisis, central banks suppressed interest rates and expanded their balance sheets. During the pandemic, they did so again on an even larger scale. Governments borrowed aggressively while central banks absorbed huge quantities of sovereign debt. Financial conditions loosened whenever markets showed signs of distress.

Investors learned a lesson from this.

Whenever conditions deteriorated, support arrived.

That belief became embedded in market psychology.

The result is a market that increasingly rewards narratives about the future while paying less attention to the price attached to them. SpaceX sits at the centre of that phenomenon. Artificial intelligence sits there too. Investors are no longer simply buying businesses. They are buying optionality, possibility and technological inevitability.

History is littered with examples of what happens when markets become convinced that policy can permanently eliminate risk.

The details change. The outcome rarely does.

The Future Has Already Been Invoiced

Investors dislike comparisons with the dot-com bubble because the comparison feels unfair.

The argument usually begins with a sensible observation. Today’s technology leaders generate enormous revenues, vast cash flows and dominant market positions. They are clearly more substantial businesses than many of the speculative internet start-ups that came to market in 1999.

All of that is true.

It is also beside the point.

The internet boom was not a story about fraudulent technology. The internet transformed the global economy. Most of the grand predictions eventually proved correct. E-commerce exploded. Cloud computing emerged. Digital advertising reshaped media. The underlying vision was remarkably accurate.

The problem was valuation.

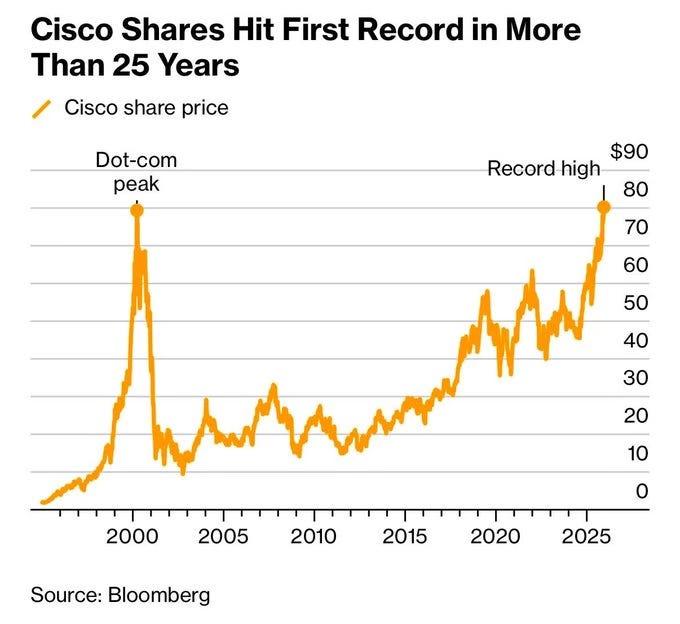

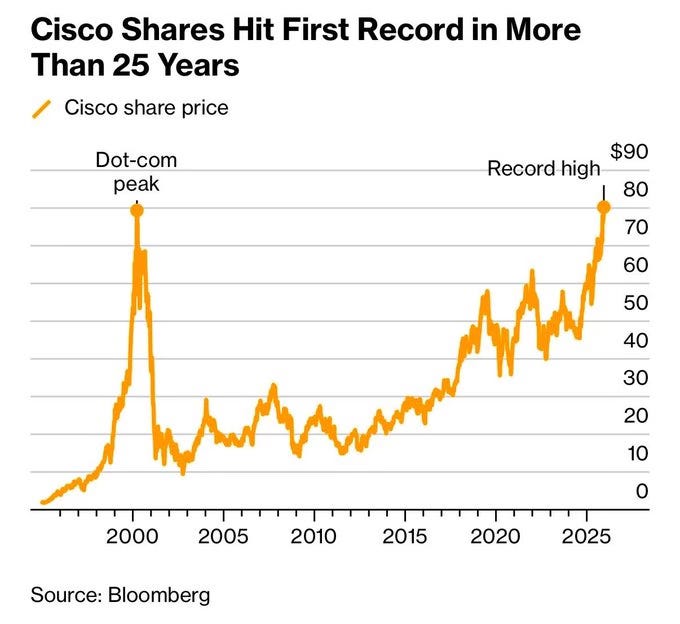

Cisco became one of the most successful technology companies in history. Yet investors who bought the stock at the peak waited 25 years to recover their losses. The same pattern appeared across much of the sector. The technology changed the world. The prices investors paid assumed it would happen immediately and without interruption.

That helps explain why the parallels with today keep resurfacing.

The resemblance has less to do with the technology itself and more to do with investor behaviour.

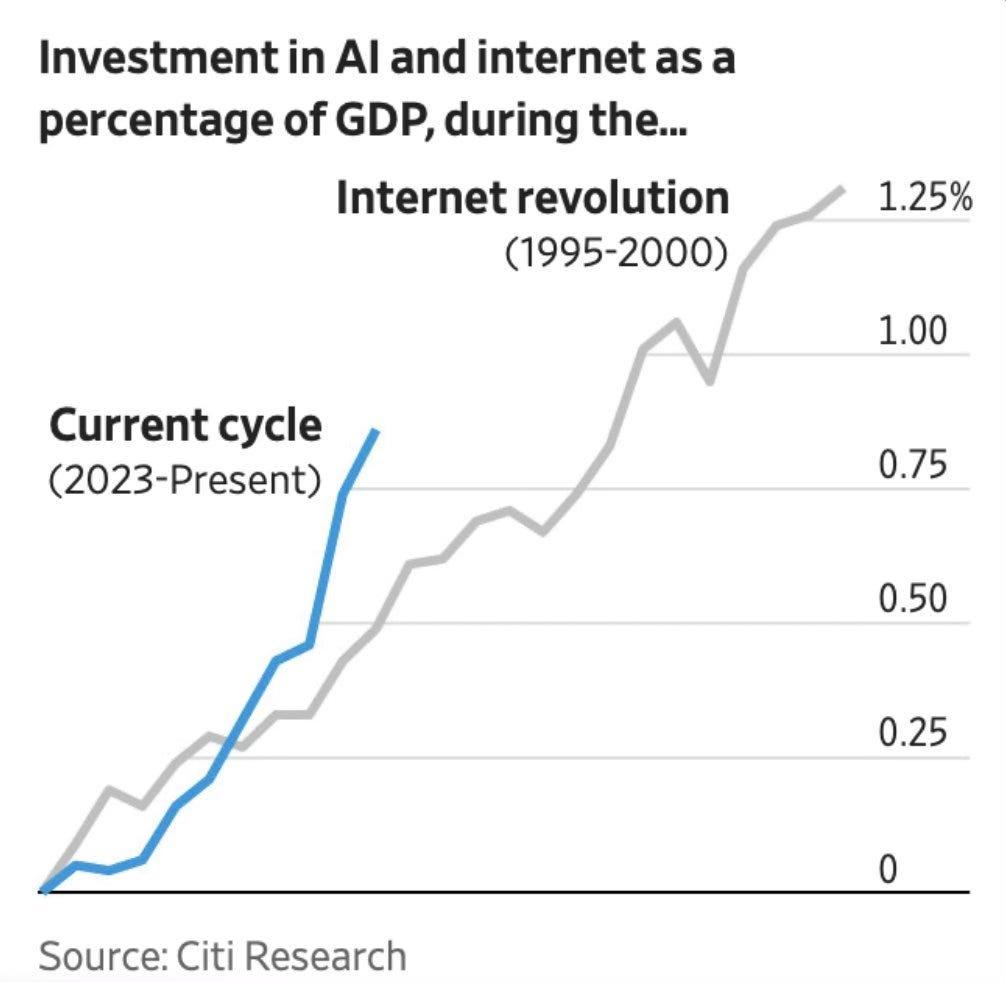

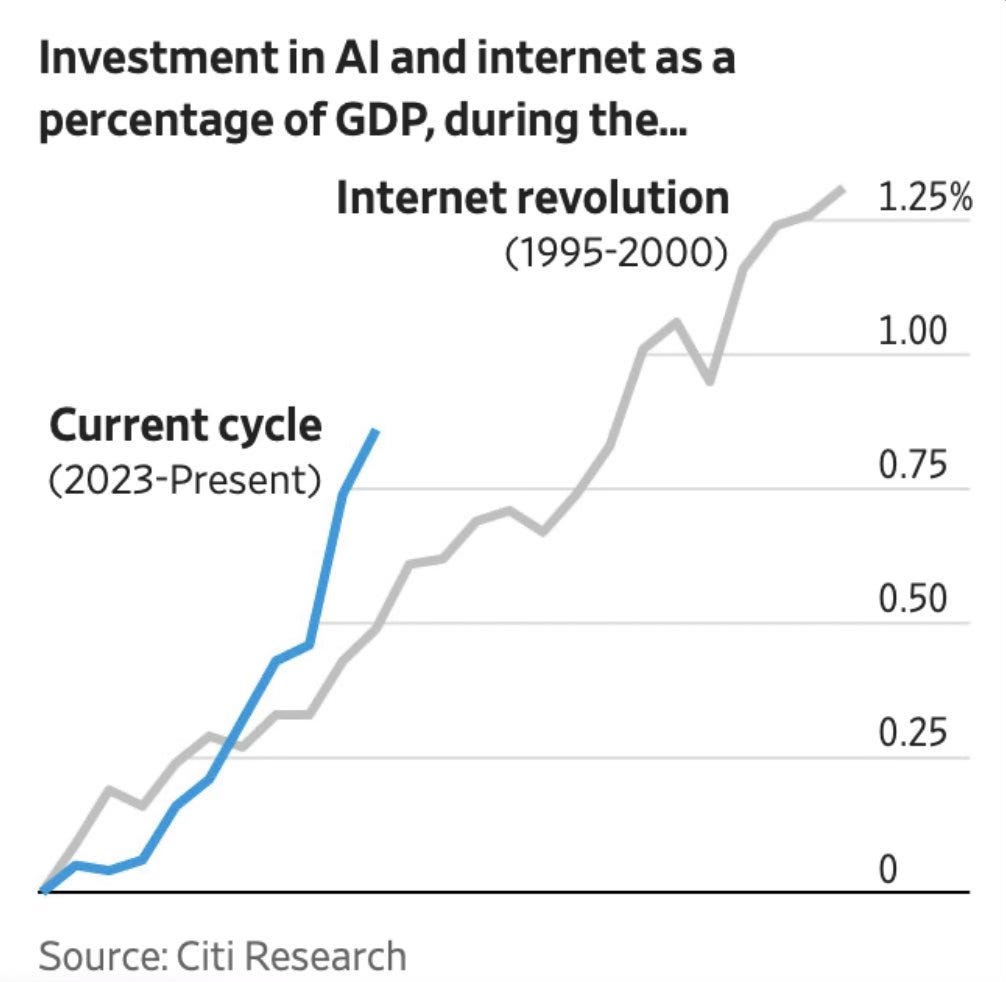

Once again, markets are looking at a genuinely transformative innovation and projecting enormous possibilities into the future. The harder question—and the one receiving far less attention—how much of that future investors have already paid for?

Source: Bloomberg, 2025

The Company Everyone Wants To Believe In

Artificial intelligence may prove every bit as revolutionary as its advocates claim.

Productivity could surge. Entire industries could be rebuilt. Economic growth may accelerate in ways that are difficult to model today.

SpaceX represents a similar idea.

Whether the conversation revolves around Mars, reusable rockets, satellite networks or AI infrastructure, investors are effectively purchasing exposure to a future they desperately want to arrive.

That desire creates distortions.

The stronger the narrative becomes, the easier it becomes to justify almost any valuation. Future revenues become present revenues. Potential market share becomes assumed market share. Success is treated as a certainty rather than a possibility.

Narratives like this have a tendency to feed on themselves.

Rising prices reinforce confidence. Confidence attracts more capital. More capital pushes prices higher.

The danger is that enthusiasm becomes a substitute for analysis.

Valuations Built on Forecasts of Forecasts

The remarkable thing about modern markets is how much confidence they continue to display despite increasingly strained fiscal realities.

Governments across the developed world are running deficits that would once have been associated with recessions or wars. Debt burdens continue rising. Interest payments are consuming larger shares of public expenditure. Bond investors have noticed. Long-term yields remain elevated despite repeated expectations of rate cuts.

Equity investors, meanwhile, remain largely focused elsewhere.

Markets are effectively making several assumptions simultaneously. Inflation will remain manageable. Economic growth will remain resilient. Governments will continue financing enormous borrowing requirements without consequence. Central banks will retain credibility. Corporate earnings will justify elevated valuations.

Perhaps all those assumptions prove correct.

Markets occasionally enjoy periods where everything goes right.

The difficulty emerges when asset prices leave little room for anything to go wrong.

The Asset Outside the System

This is where gold enters the conversation.

Gold does not require confidence in earnings forecasts, government budgets, monetary policy or technological disruption. It does not depend on a chief executive delivering another quarter of exceptional growth. It does not rely on policymakers successfully managing debt burdens that continue to climb across much of the developed world.

Its appeal comes from sitting outside that entire structure.

For years, many investors viewed gold as a defensive asset suitable only for periods of crisis. Yet the investment case increasingly looks less defensive and more practical. If markets are being supported by expanding debt, persistent deficits and repeated monetary intervention, then owning an asset with a fixed supply becomes less a speculative wager and more a form of financial insurance.

Investors seem comfortable with one form of uncertainty but not the other.

Many are willing to assign extraordinary valuations to businesses based on projections stretching a decade into the future. Yet they remain hesitant to own an asset that has preserved purchasing power through inflationary episodes, sovereign defaults, banking crises and monetary experiments spanning centuries.

That preference says something about modern markets.

The future attracts attention.

Protection rarely does.

The Difference Between Innovation and Speculation

None of this requires a bearish view on technology.

SpaceX may continue rewriting the economics of space travel. Artificial intelligence may deliver productivity gains that exceed current expectations. New industries will emerge. Some companies will justify valuations that today appear ambitious.

Innovation deserves admiration.

What deserves scrutiny is the growing tendency to assume that innovation automatically validates any price attached to it.

Markets have a habit of blurring the line between those two ideas.

Back on that launch pad in Texas, the crowd gathered because they wanted to witness the future. For a few minutes, the impossible appeared tangible. It is difficult not to be captivated by that.

Investors are experiencing something similar today. Artificial intelligence, robotics and space technology offer a vision of the future that is genuinely compelling.

SpaceX has become the perfect symbol of that optimism.

The company may justify every ounce of enthusiasm surrounding it. It may eventually exceed even the most ambitious expectations attached to it today.

History suggests that does not necessarily protect investors.

The railway companies built railways. The internet changed the world. Transformative technologies have often delivered exactly what their supporters promised. The disappointment usually arrives elsewhere. Investors become so captivated by what is possible that they stop asking what they are paying for it.

The charts comparing equities with gold pose an uncomfortable question. Have markets become more valuable, or has money become less valuable?

The answer may determine whether today’s enthusiasm is remembered as a technological revolution, a valuation bubble, or a mixture of the two.

That answer will not be found in a rocket launch, an AI model or a central bank statement.

It will be found in the price investors were willing to pay while they were watching the future leave the launch pad.

If you are considering owning physical precious metals, including gold, silver, platinum or palladium, you can explore your options through www.goldwise.com — where the focus is on ownership, security and transparency.

We are continuing to build Goldwise with content that helps investors understand what is really happening beneath the surface. If there are specific topics you would like us to break down further, or areas you feel are not being covered clearly enough, let us know.

This content is provided for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any investment. The value of precious metals can fall as well as rise, and you may get back less than you invest. Past performance is not a reliable indicator of future results. You should conduct your own research and, where appropriate, seek advice from a qualified financial adviser.

{kind=link}

{kind=link}

{kind=link}

{kind=link}