Silver’s recent sell-off suggested demand was fading. China’s behaviour suggests something very different.

There is an old survival story sailors used to tell about lifeboats in the North Atlantic.

When a ship started taking on water, panic never began when passengers noticed the damage.

It began when crew members quietly started lowering the boats before anyone else realised the ship was sinking.

That was the signal. Not the shouting above deck. Not the reassurances.

The people closest to the structure always moved first.

The silver market is beginning to look the same.

In June, silver had fallen almost 55% from its January high of $121/Oz. Investors assumed the story had changed. Higher Treasury yields, a stronger dollar and fears that Federal Reserve Chair Kevin Warsh might keep tightening policy pushed the metal to its weakest level in eight months.

Then the market changed its mind. Speaking in Sintra, Portugal, Warsh struck a noticeably less hawkish tone than markets had spent weeks preparing for. Softer US employment data followed. The dollar retreated from fourteen-month highs. Silver recovered more than 6% in a single week.

Markets had spent weeks preparing for another round of tightening. By Thursday afternoon, that assumption already looked stale.

Prices fell. Buying didn’t.

While traders were selling futures contracts, something very different was happening beneath the surface.

China was buying.

Aggressively.

When Price and Reality Part Ways

Prices tell you what traders believe today. They tell you surprisingly little about what manufacturers need next month.

Most of the time, price and reality travel together. Occasionally they don’t.

A hedge fund buys silver because it expects prices to rise. A manufacturer buys silver because the factory stops without it. The two markets often look identical.

China’s latest trade figures matter far more than the next argument over whether the Fed cuts in July or September. Silver imports have surged to their highest levels in almost a decade. At the same time, Beijing has tightened restrictions on refined silver exports.

Governments reveal priorities in speeches.

Supply chains reveal them in shipments.

When China starts importing more silver while making less of it available abroad, it is usually worth asking why. Countries rarely hoard materials they expect to become easier to replace.

The market still values silver by the ounce. China increasingly appears to value it by the decade.

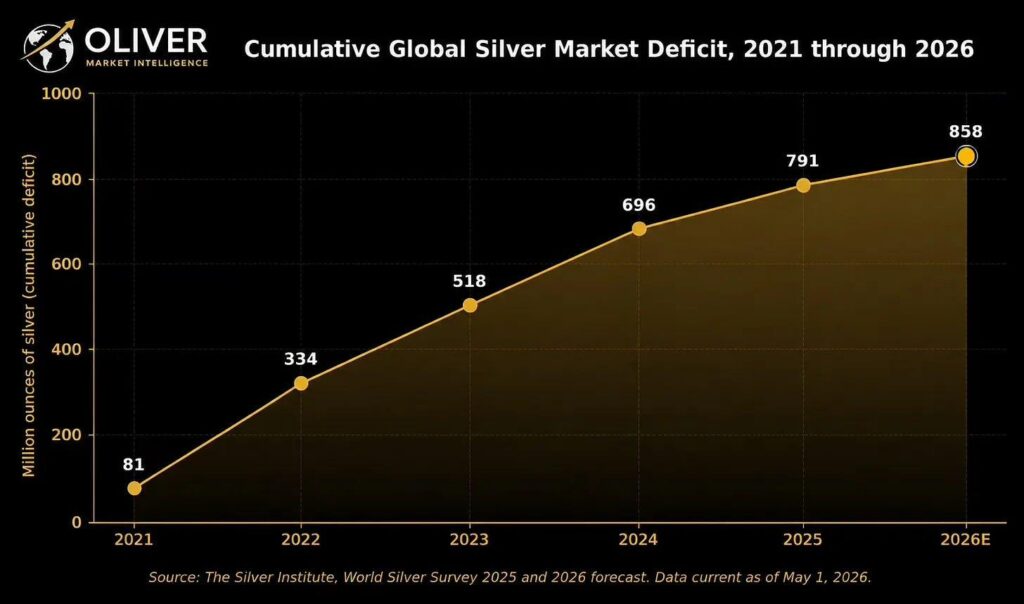

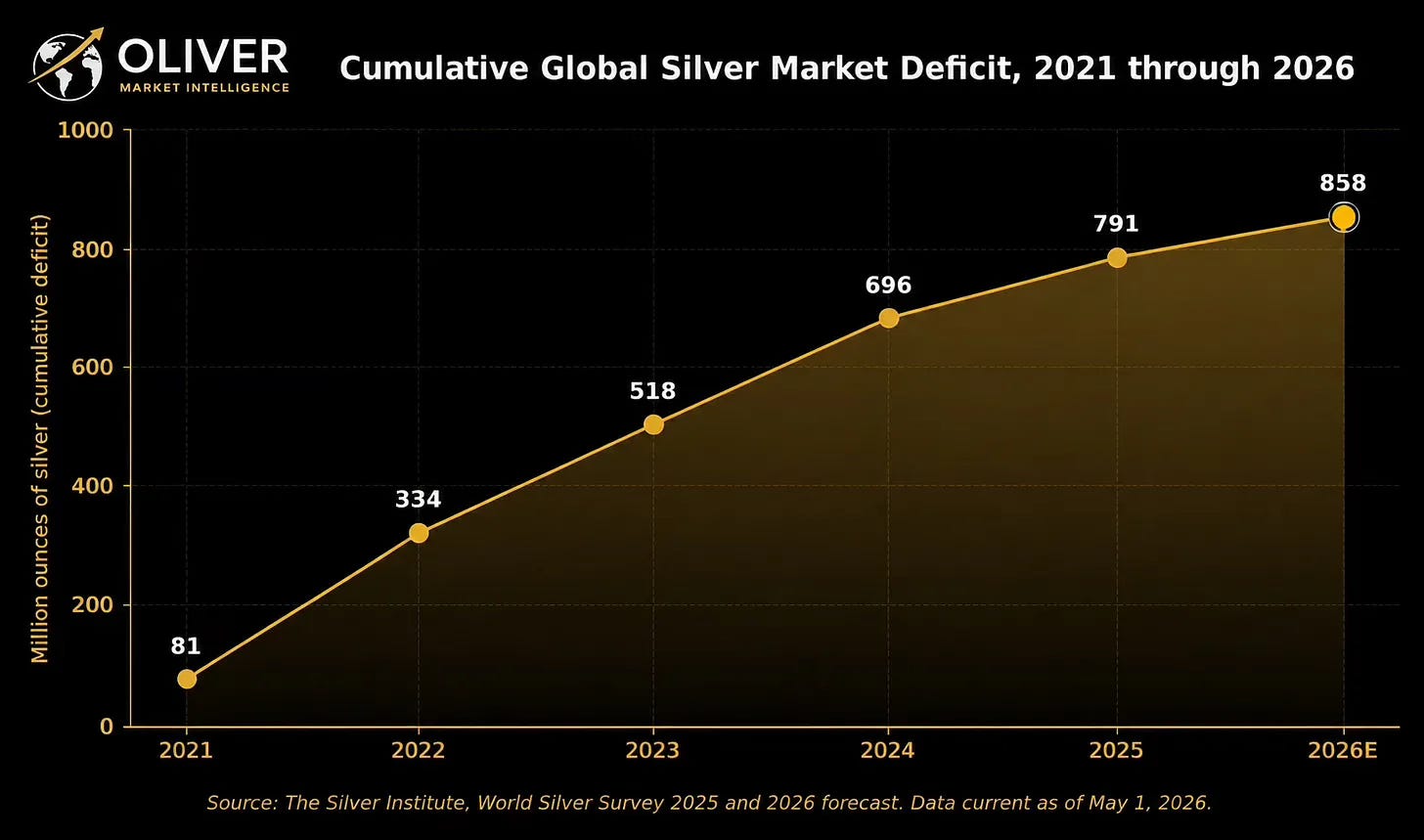

Source: Oliver Market Intelligence

The Market Is Looking in the Rear-View Mirror

One reason silver continues to surprise investors is that many are still analysing it through an old framework. They expect it to behave like a precious metal, rising and falling with inflation expectations, real yields or the strength of the dollar.

Those relationships haven’t disappeared. They’ve become less dominant.

Silver increasingly occupies two worlds at once. Financial markets still trade it as a macro asset. Industry increasingly consumes it as a critical input. One market asks whether the Federal Reserve will cut rates before Christmas. The other asks whether enough material will be available five years from now.

Those are very different questions.

Markets spend most of their time pricing the next quarter.

Manufacturers spend theirs planning the next decade.

When those two horizons drift apart, prices can become surprisingly poor guides to what is happening underneath.

Watch What Beijing Does

Commodity shortages rarely begin with empty warehouses. They begin with governments deciding tomorrow’s supply is too valuable to sell today.

That is why China’s recent behaviour matters. For decades, investors thought about silver as gold’s more volatile cousin—a precious metal that tended to perform when inflation accelerated or financial markets became nervous.

Silver has quietly changed jobs.

It used to sit alongside gold.

Now it increasingly sits alongside semiconductors.

These industries have little in common except for one critical requirement: exceptional electrical conductivity.

Industry still reaches for silver whenever conductivity actually matters.

Roughly three-quarters of global silver production arrives as a by-product of mining copper, zinc and lead. Producing significantly more silver often requires producing more of those metals first, regardless of whether those markets need additional supply.

Financial markets respond to quarterly expectations.

Geology works on a very different timetable.

Source: Oliver Market Intelligence

Eventually Someone Wants the Metal

During the liquidity panic of 2020, paper silver collapsed alongside equity markets while bullion dealers struggled to keep coins and bars in stock. The price suggested abundance. The physical market suggested the opposite.

The retail-driven silver squeeze the following year briefly exposed the same fault line. Investors focused on futures prices. Dealers focused on inventory.

Different markets. Same metal.

Prices move because opinions change.

Inventories move because reality does.

Eventually someone asks for delivery.

None of this feels entirely new. Shanghai silver continues to trade at a premium to Western benchmarks.

None of this guarantees higher prices tomorrow.

It does suggest the physical market is telling a different story from the futures market.

Information Travels Unevenly

The old lifeboat story was never really about ships.

It was about information.

Passengers watched the horizon.

The crew watched the hull.

Today’s markets remain obsessed with inflation prints, Treasury auctions and the next Federal Reserve meeting. Meanwhile, China is importing more silver, exporting less of it and saying almost nothing.

That tells us rather more than another debate over twenty-five basis points.

Markets react to headlines.

Supply chains reveal priorities.

History has a habit of rewarding the second.

If you are considering owning physical precious metals, including gold, silver, platinum or palladium, you can explore your options through www.goldwise.com — where the focus is on ownership, security and transparency.

We are continuing to build Goldwise with content that helps investors understand what is really happening beneath the surface. If there are specific topics you would like us to break down further, or areas you feel are not being covered clearly enough, let us know.

This content is provided for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any investment. The value of precious metals can fall as well as rise, and you may get back less than you invest. Past performance is not a reliable indicator of future results. You should conduct your own research and, where appropriate, seek advice from a qualified financial adviser.

{kind=link}

{kind=link}

{kind=link}