Gold still speaks London, but the next chapter may be written closer to China

There is an old joke in commodity markets that gold never really moves. It merely changes whose vault it sits in.

For decades, that joke contained an uncomfortable truth. The world could mine gold in Australia, refine it in Switzerland, sell it to a central bank in Asia and store it in London. The metal travelled thousands of miles, yet the centre of gravity never seemed to shift. The trade always found its way back to the same place.

London became the gold market’s nervous system long before most modern financial centres existed. Its clearing infrastructure, vault network and institutional relationships created something remarkably durable: trust. Not trust in gold itself. Gold does not need trust. Trust in the machinery around it.

What makes 2026 interesting is not simply that gold prices have surged again. Markets have spent centuries oscillating between enthusiasm and indifference towards the metal. What feels more consequential is that the infrastructure itself is beginning to move.

The Asset Nobody Can Sanction

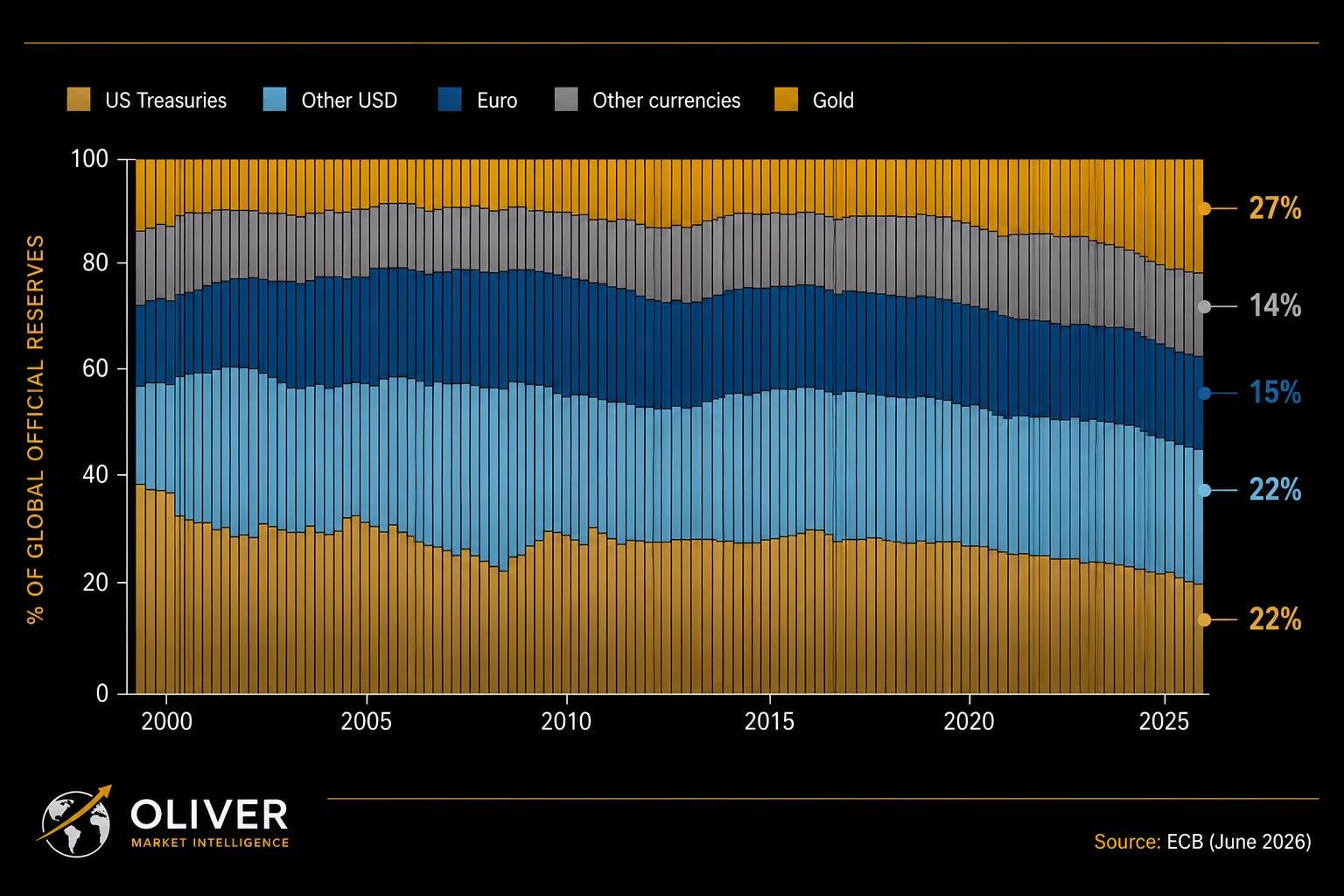

The latest signal came from the European Central Bank. According to new ECB data, gold has overtaken US Treasuries as the world’s largest reserve asset, accounting for 27 per cent of global central bank reserves at the end of 2025, compared with 22 per cent for Treasuries. Central banks now collectively hold more than 36,000 tonnes of gold, approaching levels last seen during Bretton Woods. The largest buyers since 2022 have included China, India, Turkey and Poland. This is too broad and persistent to dismiss as portfolio housekeeping. It reflects something deeper in the monetary system.

Reserve managers rarely speak the language of politics. Their actions often do.

The freezing of Russia’s foreign reserves after the invasion of Ukraine was initially treated as a singular geopolitical event. It now looks more like a turning point in reserve management. Assets that can be frozen carry a different kind of risk from assets that can fall in price. One is financial. The other is political.

Gold looks different through that lens. Unlike sovereign bonds, it has no issuer. Unlike reserve currencies, it carries no dependency on another government’s policy choices. It does not generate income, but it does offer something that has become increasingly valuable in a fragmented world: neutrality.

That helps explain why central banks have been accumulating bullion at the fastest pace in decades. Yet buying gold is only part of the story. Holding more gold eventually forces countries and institutions to ask a practical question.

Where should it be stored, settled and cleared?

That question is becoming harder to answer with London alone.

Source: Financial Times

The Plumbing Matters More Than the Price

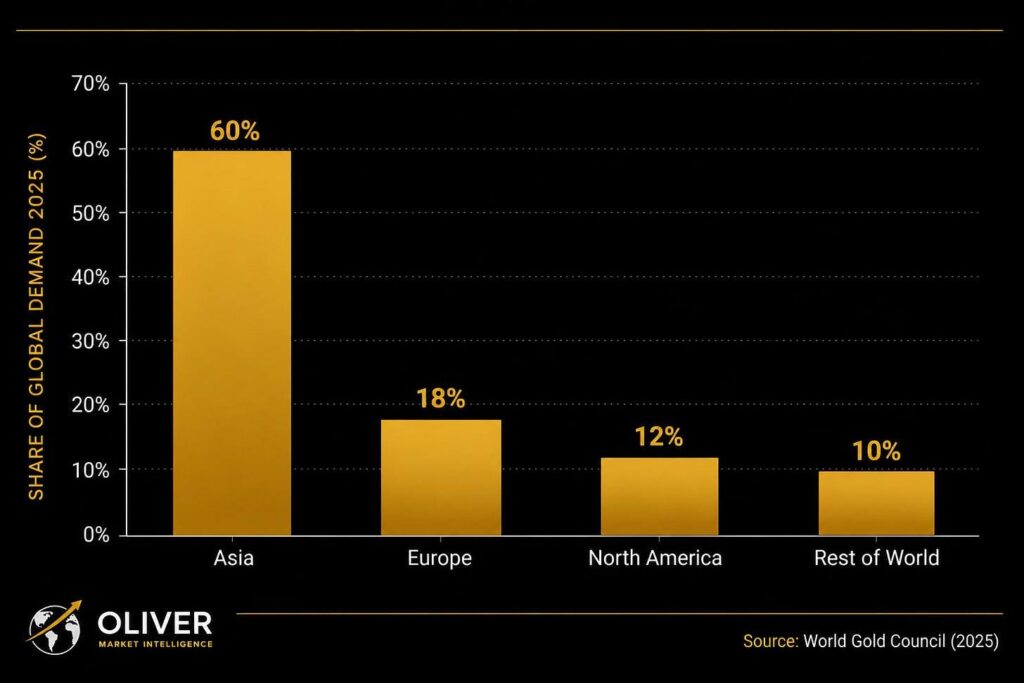

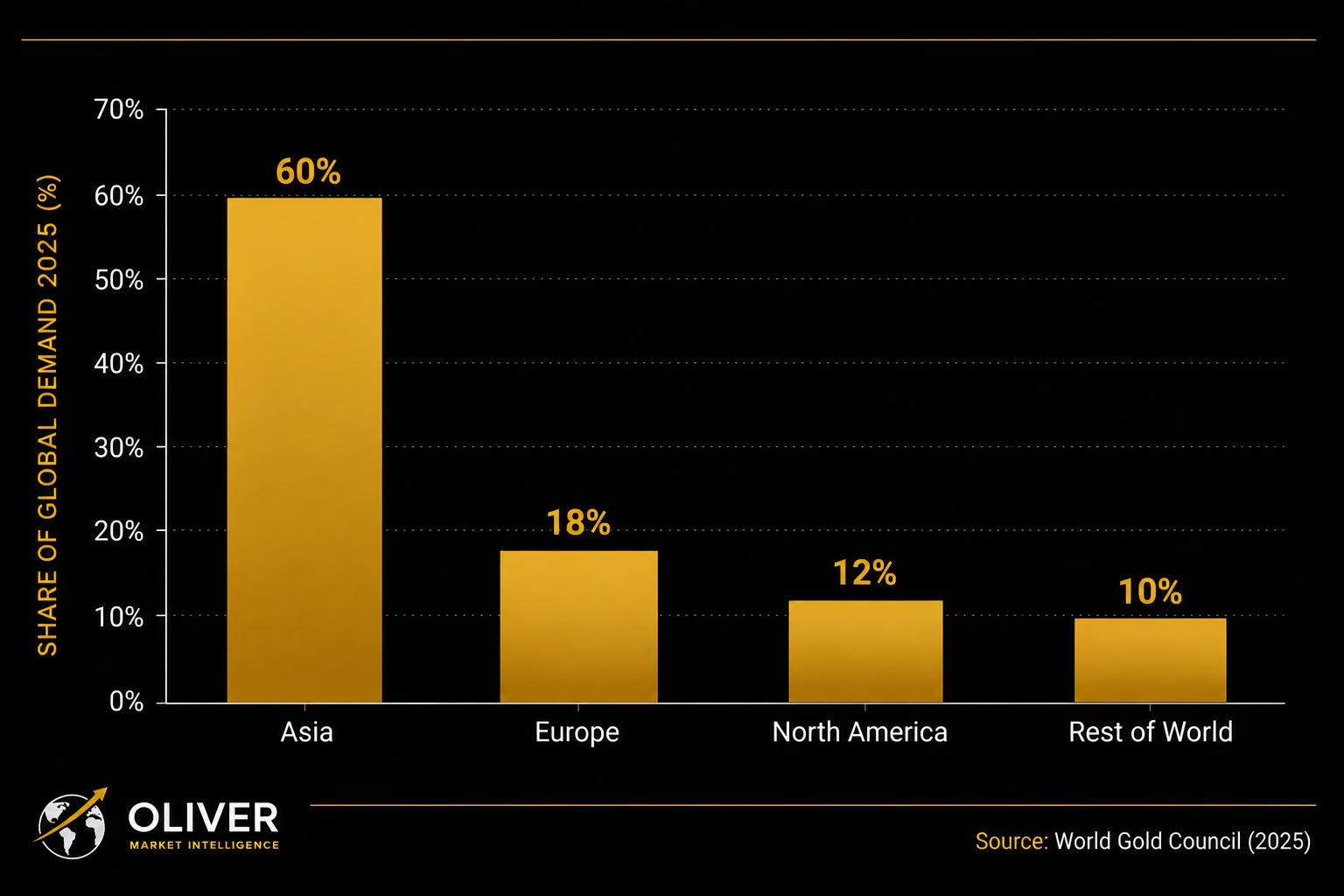

The strange reality of the modern gold market is that Asia accounts for roughly 60 per cent of global physical demand, yet the mechanisms that price, clear and settle gold remain overwhelmingly Western. The benchmark infrastructure was built around the needs of London and New York, even as physical flows increasingly pointed east.

For years, that mismatch was tolerated because the existing system worked.

Now Asia is beginning to build its own.

Hong Kong plans to launch a new gold clearing system as early as July through the Hong Kong Precious Metals Central Clearing Company, developed in partnership with the Shanghai Gold Exchange. The ambition is straightforward: replicate the institutional efficiency of London’s over-the-counter clearing system while anchoring it inside Asia’s own financial ecosystem. The project is supported by vault expansion plans, logistics infrastructure and direct connectivity to mainland China’s gold market.

Gold clearing sounds like obscure market plumbing. In reality, it is where much of the power resides.

Most institutional gold transactions do not involve bars physically changing hands. Ownership is transferred electronically through clearing systems, with positions netted against one another. The process reduces costs, improves liquidity and creates a market large enough to support global trading.

The institutions that control clearing infrastructure do not merely facilitate transactions. They shape where liquidity gathers.

Markets are gravitational systems. Liquidity attracts liquidity.

London understood this centuries ago. Hong Kong understands it now.

Source: World Gold Council, Oliver Market Intelligence

Why Asia Wants Its Own Gold Market

The significance of Hong Kong’s initiative extends beyond efficiency. What makes it different from previous attempts is its connection to China. The partnership with the Shanghai Gold Exchange provides access to the world’s largest physical gold consumer and one of its largest official accumulators. For international institutions seeking exposure to Chinese gold demand without operating directly inside mainland markets, Hong Kong becomes an obvious bridge.

Singapore is pursuing a similar path, though with its usual preference for patience over spectacle. The Monetary Authority of Singapore has assembled a consortium that includes JPMorgan, UBS, DBS and ICBC Standard Bank to build its own clearing architecture. Singapore’s pitch is different. Hong Kong offers proximity to China. Singapore offers neutrality.

That difference matters. One city benefits from access to China’s economic scale. The other benefits from remaining outside China’s political orbit. Both propositions have customers.

What neither city is really competing against is the other.

They are competing against an assumption.

For decades, the assumption was that the world’s gold market would remain permanently organised around Atlantic financial centres. Physical demand could migrate east, reserve accumulation could migrate east, refining capacity could migrate east, but the settlement infrastructure would remain where it had always been.

That assumption is beginning to look old.

Source: ECB, Oliver Market Intelligence

The Long Journey Home

During the nineteenth century, financial power followed trade routes. London’s dominance was not created by financial innovation alone. It emerged because Britain sat at the centre of global commerce. Capital eventually built itself around those flows.

The same process may now be occurring in reverse.

As more gold is purchased by Asian central banks, sovereign wealth funds and investors, there is growing logic to settling that gold closer to where it ultimately resides. Geography matters. Time zones matter. Regulatory frameworks matter. Market infrastructure rarely remains detached from the underlying flow of assets forever.

None of this means London is about to lose its position. Financial centres tend to decline gradually, not suddenly. London’s clearing ecosystem has centuries of institutional memory, deep liquidity and entrenched relationships. Those advantages are real.

Yet history is full of systems that appeared permanent until the economics underneath them changed.

Gold itself is sending a message.

The ECB’s data showing bullion overtaking US Treasuries as a reserve asset is striking not simply because of what it says about gold. It reveals something about confidence. The post-Cold War era was built around the assumption that financial globalisation would continue expanding under a largely unified framework. Reserve managers now appear to be preparing for a different world.

A world where ownership matters, location matters and neutrality carries a premium.

That is why Hong Kong’s clearing ambitions deserve attention. They are not just about bullion trading. They represent an attempt to build the infrastructure for a different monetary geography.

Perhaps the most telling detail is that nobody involved is presenting this as a revolution. Officials speak about efficiency, connectivity and market development. Major changes in financial systems rarely arrive with grand declarations. They arrive disguised as administrative upgrades and clearing mechanisms.

The old joke said gold never really moves.

Looking around today, that feels less convincing than it once did.

The bars may still sit quietly inside vaults. The ownership records may still move through electronic ledgers. Yet something larger appears to be shifting beneath them.

For centuries, the world’s gold found its way back to London. Now the metal is accumulating elsewhere, the reserves are accumulating elsewhere, and increasingly the infrastructure is being built elsewhere too.

The vault doors have not moved yet.

But the map around them has.

If you are considering owning physical precious metals, including gold, silver, platinum or palladium, you can explore your options through www.goldwise.com — where the focus is on ownership, security and transparency.

We are continuing to build Goldwise with content that helps investors understand what is really happening beneath the surface. If there are specific topics you would like us to break down further, or areas you feel are not being covered clearly enough, let us know.

This content is provided for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any investment. The value of precious metals can fall as well as rise, and you may get back less than you invest. Past performance is not a reliable indicator of future results. You should conduct your own research and, where appropriate, seek advice from a qualified financial adviser.

{kind=link}

{kind=link}

{kind=link}