Gold Moves When the Rules Change

From Sutter’s Mill to digital currencies, this is the story of how monetary systems evolve and where trust moves next.

On 24 January 1848, at Sutter’s Mill in California, James Marshall found gold in the South Fork of the American River. Within months, the discovery triggered one of the largest migrations in modern history. Hundreds of thousands of people moved west, not in search of wages or opportunity in the modern sense, but in search of something far more fundamental.

They were searching for money itself.

Gold did not need to be issued, verified, or authorised. It could be held, traded, and recognised anywhere. That was its power. Not speed or convenience, but finality. When a transaction was settled in gold, it was complete. No third party was required, and no system needed to remain operational for it to retain value.

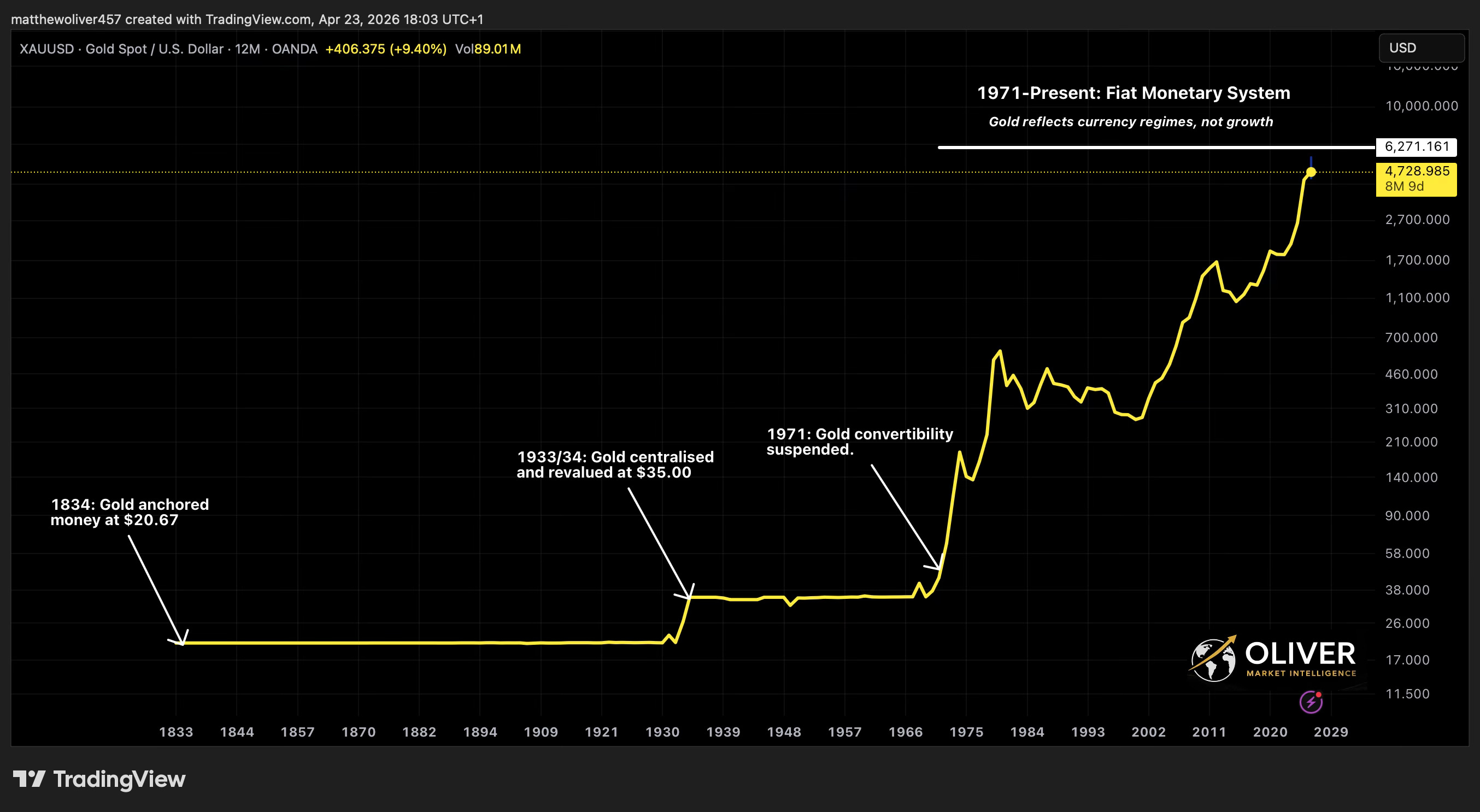

At the same time, the United States was formalising this reality into law. The Coinage Act of 1834 adjusted the gold content of U.S. coin, the Mint Act of 1837 standardised it, and by 1900 the Gold Standard Act defined the dollar explicitly in terms of gold. The result was a system where money was anchored to something scarce, with an official parity of roughly $20.67 per ounce.

From 1834 to 1933, this framework imposed discipline. Governments and banks could expand credit, but they remained tied to an external constraint. Money could not be created without limit because it ultimately had to reconcile back to gold.

But that constraint came with a cost.

Gold discovered at Sutter’s Creek, 1848

When the System Could No Longer Hold

By the late 19th century, the tension was already visible. In 1896, William Jennings Bryan delivered his “Cross of Gold” speech, arguing that the gold standard restricted economic growth and placed pressure on debtors. His argument was not really about gold itself, but about what happens when money is tied to something that cannot expand easily.

Gold won that political battle. The Gold Standard Act of 1900 reaffirmed the system and formalised the dollar’s link to gold.

But the underlying pressure never disappeared.

It returned with force after the Wall Street Crash of 1929 and the onset of the Great Depression, when collapsing banks, falling prices, and rising unemployment pushed the monetary system to breaking point. The gold standard, once seen as a source of stability, became a constraint that limited how governments could respond to the crisis.

In 1933, that tension reached its limit. Roosevelt intervened decisively. Private gold ownership was effectively ended through forced exchange, and control over gold was transferred to the state. Shortly after, gold was revalued from $20.67 to $35 per ounce.

This was not a collapse. It was a reset.

Gold remained in the system, but no longer in the hands of the public. Control had moved upward.

That structure continued into Bretton Woods, a post-World War II monetary framework in which global currencies were linked to the U.S. dollar, while the dollar itself remained tied to gold at $35 per ounce. In practical terms, countries no longer used gold directly for trade, but relied on the dollar as a proxy for it.

For most people, the connection to gold had already disappeared.

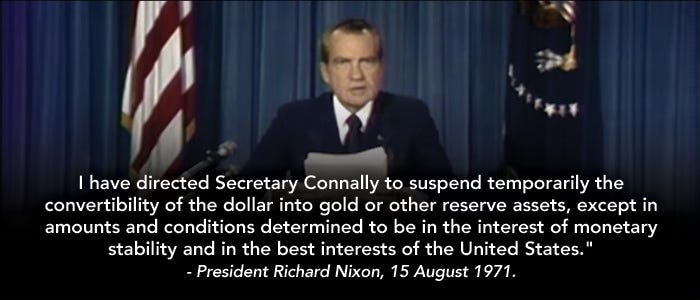

Then, in 1971, the final link was removed. Nixon closed the gold window, ending convertibility altogether. From that point forward, the dollar and the global monetary system operated without any anchor to a scarce asset.

Money became entirely dependent on policy, confidence, and institutional trust.

“Temporarily.”

What Changed in the Structure of Money

At first glance, the story of money appears to be one of progress. Systems become more efficient, transactions become faster, and new forms of money emerge with improved functionality.

But beneath the surface, the change is more structural.

The unit of money itself has been weakening over time.

This follows a pattern seen across monetary history. Systems begin with constraint, move toward flexibility, and eventually require increasing levels of management to maintain stability. Gold imposes discipline because it cannot be created arbitrarily. Fiat removes that constraint, allowing expansion in response to economic pressure.

That expansion can be useful in the short term. It enables growth, absorbs shocks, and supports financial systems. Over time, however, it can introduce instability. As liquidity increases and confidence becomes more fragile, the system compensates by adding layers of oversight and control.

Trust moves accordingly. It shifts from the asset itself to the institutions managing it, and increasingly to the infrastructure that supports those institutions.

Each step improves convenience.

Each step increases dependency.

A Pattern That Keeps Repeating

This sequence has repeated across major monetary transitions.

Gold anchored the system through the 19th and early 20th centuries. That anchor created stability, but also limited expansion. Political and economic pressure built over time, eventually leading to intervention in 1933. The system was adjusted, not abandoned, with gold centralised and revalued.

By 1971, the same pressure had reappeared at the global level. The United States needed to supply liquidity to the world, but could no longer maintain the gold link while doing so. Once again, the constraint was removed.

The pattern is consistent.

A system is anchored to something real.

That anchor creates both stability and limitation.

Pressure builds as the system expands.

The state intervenes to relieve that pressure.

The anchor is weakened or removed.

Control shifts upward.

Gold did not fail in these transitions. It was removed because it imposed limits that the system could no longer accommodate.

“Gold reflects currency regimes, not growth.” -Oliver Market Intelligence

The Next Phase of Money

Today, we are watching the next phase of this process unfold.

The trigger was blockchain and, above all, Bitcoin. For the first time, value could be transferred without a central intermediary. That opened two competing paths: one driven by decentralised technology seeking to separate money from control, and the other by central banks seeking to retain it.

Stablecoins sit within this shift as a growing focus: digital extensions of fiat that enable movement within digital markets while remaining dependent on reserves, issuers, and regulation.

At the same time, central banks are accelerating their response. From a potential digital pound in the UK to ongoing Federal Reserve research and cross-border initiatives, the direction is clear. Alongside this, central banks continue to accumulate gold.

On the surface, this appears to be about efficiency. Faster payments, lower costs, broader access. But underneath, the structure of money is changing again.

Money is being rebuilt as infrastructure.

Stablecoins may act as a transitional layer, bridging traditional currency and digital systems. CBDCs represent a further step: not private instruments linked to fiat, but direct digital forms of state-issued money, with the potential for programmability embedded into the system itself.

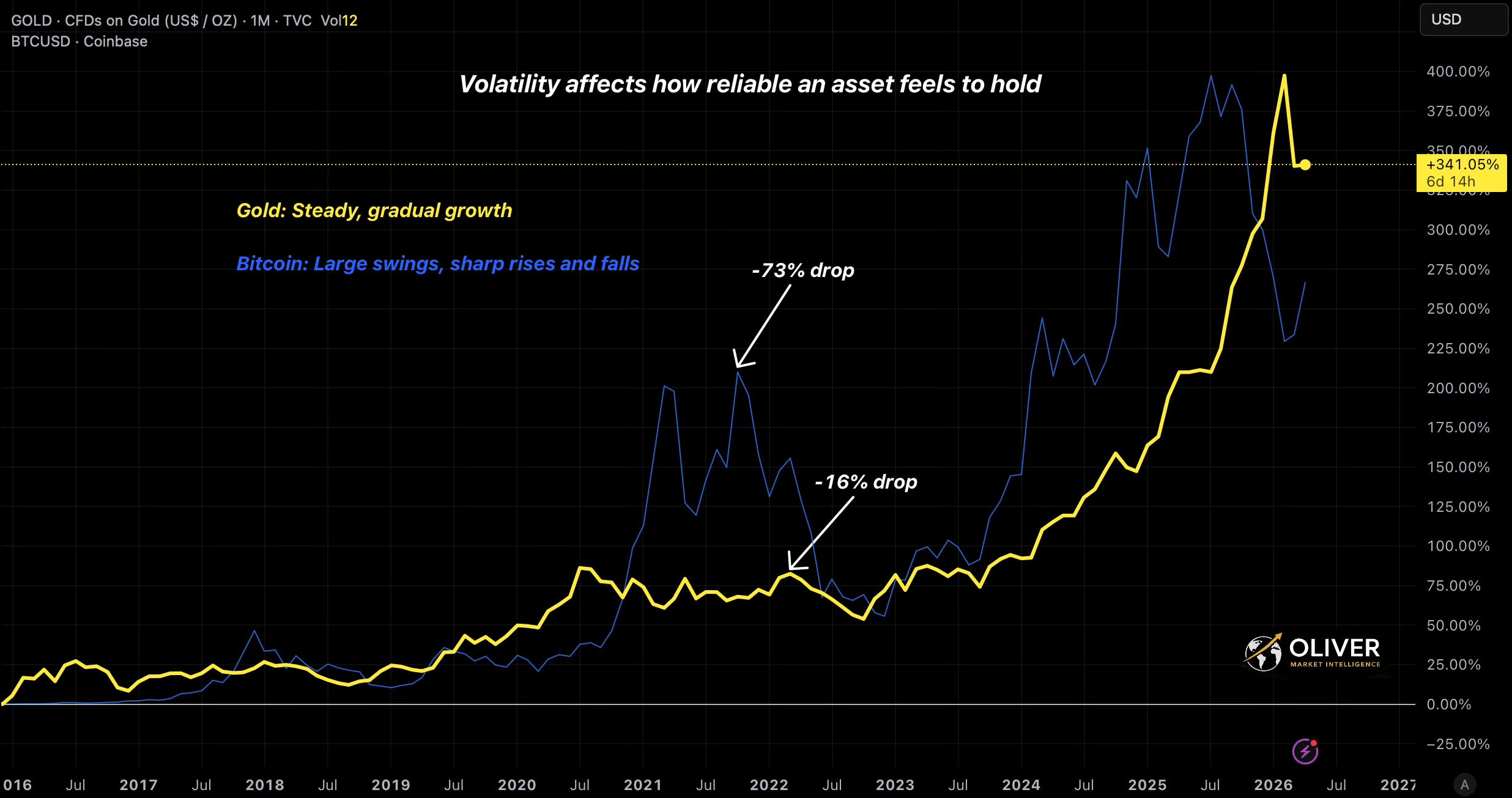

Bitcoin, meanwhile, was framed as a form of “digital gold.” In practice, it has behaved very differently, characterised more by volatility and speculation than stability. That divergence sets up the central question that follows: what actually functions as independent money when the system is under stress?

Source: Bank of England, 2023

Cyber Risk and the Fragility of Digital Money

As money becomes more digital, it inherits the vulnerabilities of digital systems.

Recent developments around advanced cyber tools, such as the Mythos AI case, highlight how even highly controlled environments can be accessed or misused through indirect channels. These examples illustrate a broader reality in which increasingly complex systems create new forms of risk.

Digital money depends on networks, software, and access points. Exchanges can be compromised, wallets can be tracked, and infrastructure can be disrupted. The system does not need to fail entirely for trust to be affected. It only needs to fail at key points.

Gold operates outside this framework.

It does not depend on software, connectivity, or permission. It cannot be remotely accessed or digitally restricted. Its risks are physical rather than systemic.

As financial systems become more complex, that distinction becomes more relevant.

Gold, Bitcoin, and the Question of Independence

Bitcoin was introduced as a response to many of these issues, offering a decentralised system designed to reduce reliance on trust.

In practice, however, it introduces a different form of dependency.

Bitcoin remains volatile, which can make it challenging to function as a stable store of value. Its base layer is not optimised for high-volume settlement, and its transaction history is transparent and traceable. More importantly, it operates within an ecosystem that depends on exchanges, custodians, and regulatory frameworks.

It is decentralised in theory, but dependent in practice.

Gold does not share these characteristics. It does not rely on a network to validate it or an institution to maintain it. Historically, it has functioned as a system-independent store of value.

Its limitation has traditionally been mobility.

Platforms like Goldwise represent an emerging model that combines fractional ownership of allocated physical gold with digital access. This allows value to be transferred more efficiently while maintaining a connection to a physical asset.

In this structure, gold remains the underlying asset, while digital systems act as the mechanism through which it can be accessed and transferred.

“It’s not just what an asset returns — it’s what you can hold.” -Oliver Market Intelligence

Where This Leaves the Market

If this framework is correct, then the core issue is not inflation alone, but the gradual shift in how trust is structured within the monetary system.

Markets may be underestimating the fragility of increasingly complex digital infrastructure, while also underestimating the role of assets that exist outside that system.

Central banks accumulating gold, governments building digital currencies, and the growing integration of financial systems into programmable infrastructure all point to a system in transition.

The question is not simply how money evolves, but how it behaves under stress.

If digital systems become the dominant layer of money, how resilient are they to disruption, whether from cyber threats, infrastructure failure, or policy intervention?

If money becomes programmable, what happens when that programmability is used to restrict rather than enable?

And if Bitcoin and other digital assets are positioned as alternatives, can they truly operate independently of the systems that provide liquidity, access, and regulation?

Or does their reliance on infrastructure place them closer to the system they were designed to replace?

At the same time, as gold continues to play a role within central bank strategy and is increasingly integrated into modern financial rails, does it represent a return to a more stable foundation, or simply a different function within a more complex system?

These are structural questions.

And the answers will shape how money is understood in the next phase of the system.

What began at Sutter’s Mill as a search for something real now sits alongside a system built on trust, code, and policy. The balance between the two is still being decided.

If you are considering owning physical precious metals, including gold, silver, platinum or palladium, you can explore your options through www.goldwise.com — where the focus is on ownership, security and transparency.

We are continuing to build Goldwise with content that helps investors understand what is really happening beneath the surface. If there are specific topics you would like us to break down further, or areas you feel are not being covered clearly enough, let us know.

This content is provided for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any investment. The value of precious metals can fall as well as rise, and you may get back less than you invest. Past performance is not a reliable indicator of future results. You should conduct your own research and, where appropriate, seek advice from a qualified financial adviser.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}