Nominal gains are rising, but real wealth across the UK is quietly shrinking

In the mid-1970s, Britain appeared—at least on paper—to be getting richer.

Wages were rising, interest rates were high, and savers could open their passbooks and see their balances steadily increasing. It gave the impression of progress. More pounds in your account felt like more security, more stability, and more wealth.

But the reality inside British households told a very different story.

By 1975, UK inflation had surged to 24.2%, while Bank Rate sat closer to 10–11.5%. That meant even though savers were earning interest, and workers were receiving pay rises, the cost of living was rising far faster than their income or savings.

Food, fuel, housing—everything was becoming more expensive at a pace that outstripped financial gains.

This created what can only be described as a financial illusion. People were earning more, saving more, and yet falling behind. Their money was growing in number, but shrinking in value.

That same illusion is quietly re-emerging today.

1970’s Austerity, Daily Mail

A Familiar Pattern in Today’s Headlines

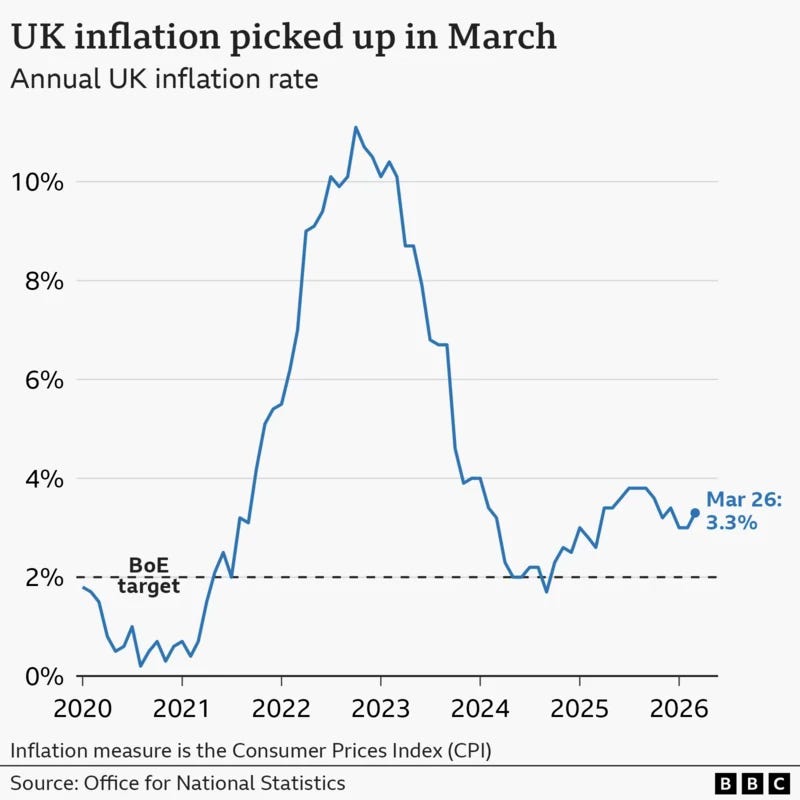

Recent UK economic data shows clear echoes of that earlier period.

Inflation has climbed to 3.3%, with rising costs in essentials like food and energy continuing to filter through the economy. At the same time, the International Monetary Fund has downgraded the UK’s growth outlook, warning that persistent inflationary pressure is weighing on economic performance.

Taken together, these developments create a challenging environment for savers.

When inflation rises while growth slows, incomes tend to stagnate while costs continue to increase. It is precisely in this kind of environment that the gap between what your money is and what it can buy begins to widen.

Source: BBC, Office for National Statistics

Nominal Returns vs Real Returns

Most people assess their financial progress by looking at whether their money has increased.

If you have £10,000 and it grows to £10,300, it feels like progress. That is a 3% nominal return—the headline figure most banks advertise.

But this figure tells only part of the story.

What actually matters is the real return, which adjusts for inflation. The Bank of England describes nominal returns as including compensation for inflation, while the European Central Bank offers a simple rule of thumb:

Real return ≈ Nominal return – Inflation

In practical terms, this means that if your money grows slower than the cost of living, you are losing purchasing power, even if your balance increases.

The Quiet Loss in Everyday Saving

Consider a simple example.

If you place £100 into a savings account paying 2% interest, you will have £102 after a year. However, if inflation is running at 3%, something that cost £100 at the start of the year now costs £103.

So although your balance has increased, your money buys less than it did before. Your real return is approximately –0.97%.

This is not an abstract concept—it reflects the current reality for many UK savers.

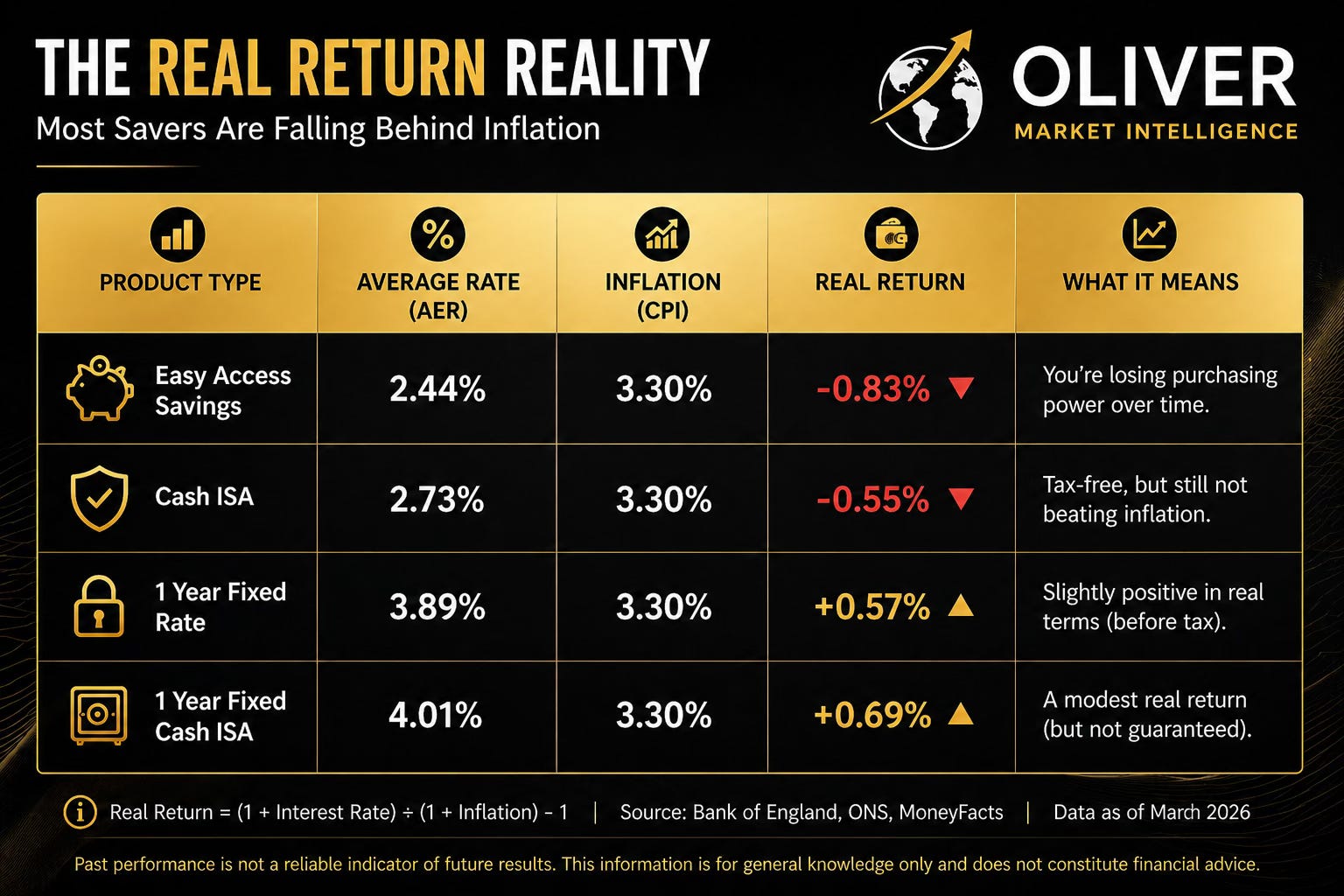

With inflation at 3.3%, and average easy-access savings rates around 2.44%, typical savers are experiencing real returns of roughly –0.83%. Even cash ISAs averaging 2.73% still fall short of inflation, producing negative real returns.

The result is a widespread but often unnoticed phenomenon: many savers are becoming poorer in real terms, despite doing what they believe is financially responsible.

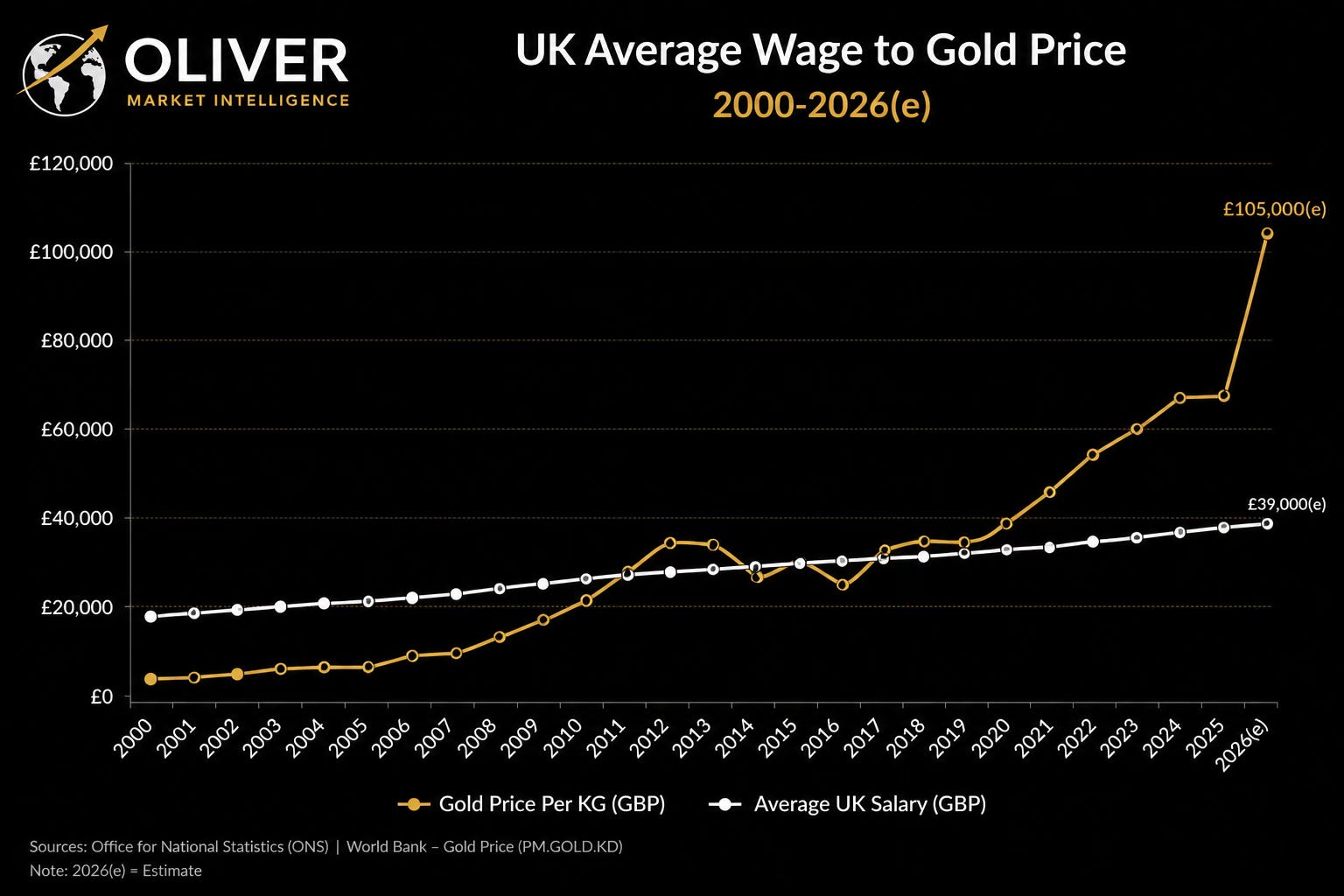

Source: Oliver Market Intelligence

When the Measuring Stick Changes

Most people think of inflation as prices going up. But there is another side to the same story: the measuring stick itself can change.

In older centuries, debasement meant reducing the precious metal in a coin. In modern Britain, it is better understood as expanding money and reserves so that each pound carries less purchasing power over time. That is not a theoretical risk. In 1949 the pound was officially devalued from $4.03 to $2.80 against the then gold-linked dollar. In 1967 it was devalued again from $2.80 to $2.40.

In 1992, sterling was forced out of the ERM after an unsuccessful defence, and George Soros became famous for profiting from the market’s view that the pound had been set at an unsustainable level.

What makes this relevant now is the scale of change since recent crises. ONS CPI data imply that a basket costing £100 in March 2020 costs about £129.83 in March 2026, so the pound has lost roughly 23% of that lockdown-era purchasing power.

Relative to September 2008, the loss is starker: today’s £100 buys only about what £61 bought then. Over the same broad period, QE reached £895 billion, the Bank’s reserves rose from roughly £25 billion in 2008 to around £654 billion even in late 2025 after the peak, and M4 broad money climbed from £1.93 trillion at end-2008 to £3.21 trillion by end-2025.

Whether you call that monetary support or monetary dilution, the practical point for savers is the same: a rising cash balance does not guarantee a stable pound.

Why It Often Feels Worse

Official inflation figures attempt to measure the average rise in prices, but they do not always reflect individual experience.

Households spend differently. For many, essential costs—such as rent, energy, and food—have risen faster than the headline rate suggests. This means personal inflation can exceed official figures.

At the same time, many savings products lag behind inflation.

The outcome is a persistent gap between nominal growth and real-world affordability. Over time, this gap compounds, gradually reducing what savings can actually achieve.

The Risk of Standing Still

Cash has traditionally been seen as a safe place to store wealth. It offers stability, liquidity, and certainty.

However, in an inflationary environment, that stability can be deceptive.

If your savings consistently earn less than inflation, you are effectively accepting a gradual loss of purchasing power. The risk is not sudden or dramatic—it is slow, steady, and cumulative.

Standing still in cash can feel safe, even as the measuring stick itself becomes less reliable.

Over years or decades, this erosion can have a meaningful impact on long-term financial outcomes, particularly for savers and retirees.

It is also important to recognise that cash still plays an essential role. Short-term needs, emergency funds, and liquidity requirements are typically best served by holding cash. The challenge arises when too much long-term wealth is left exposed to inflation without protection.

Why Gold Enters the Conversation

When the focus shifts from nominal returns to purchasing power, it changes how assets are evaluated.

In periods where currency loses value over time, attention often turns to assets that are not directly tied to monetary policy.

Gold has historically played that role.

Unlike cash, gold cannot be created by central banks. Its supply is limited, and it exists outside the traditional financial system. This gives it different characteristics to currencies that can be expanded in response to economic conditions.

When the price of gold rises in pounds, it often reflects a change in the purchasing power of the currency itself. In simple terms, it takes more pounds to buy the same amount of gold.

From this perspective, gold can act as a reference point—highlighting shifts in the value of money rather than simply moving independently.

Source: Oliver Market Intelligence

Purchasing Power vs Pound Value

The key distinction is between holding money and holding value.

Cash is designed for stability and liquidity, but its value is linked to the strength of the currency. When inflation rises, that value can decline over time.

Gold, by contrast, is not dependent on a single currency. Its value is determined globally, which means it can adjust as currencies fluctuate.

For savers concerned about the long-term purchasing power of their money, this difference becomes increasingly relevant.

Rather than focusing purely on how many pounds are held, the focus shifts to what those pounds can actually buy—and how that changes over time.

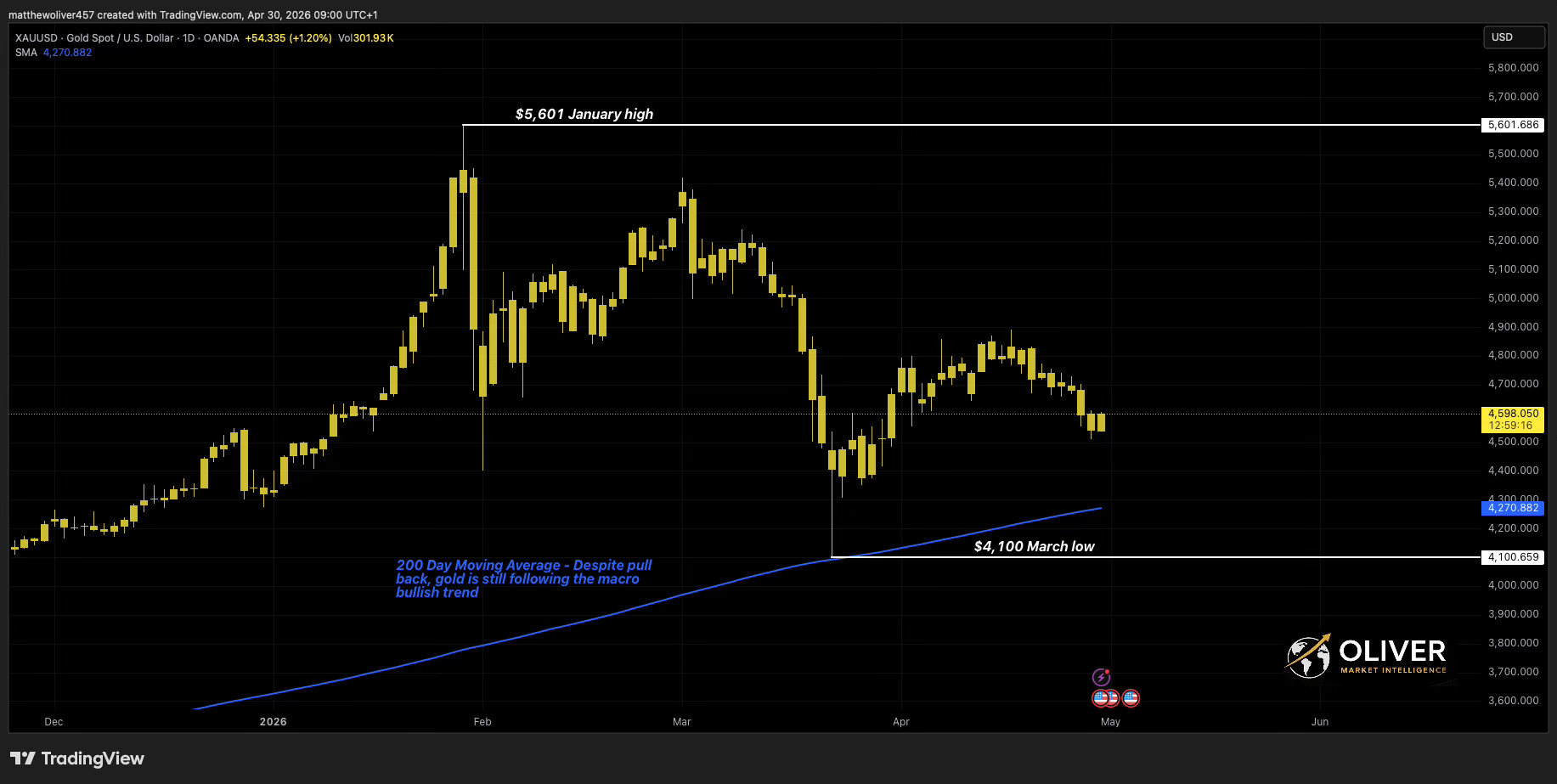

Why Gold Has Recently Fallen And Why That Matters

In recent months, something has caught many investors off guard.

Gold prices have fallen from the January high of $5,601/Oz, to as low as $4,100/Oz on the 23rd March – even as global uncertainty has remained elevated. At the time of writing, gold is now trading around the $4,600/Oz level, representing a 17.9% drop from the highs.

At the same time, bonds have become more attractive. This shift goes a long way in explaining gold’s recent weakness.

When interest rates rise, government bonds begin to offer higher yields. For investors looking for income, that creates a strong incentive to move money away from gold, which does not produce interest. As a result, some investors have reduced their gold holdings and moved into bonds.

A stronger US dollar has added further pressure, along with short-term factors such as gold sales by some countries and outflows from gold-backed funds.

However, this shift towards bonds deserves a closer look, particularly for UK investors.

Higher bond yields are not appearing in isolation. They reflect rising concerns about inflation, government borrowing, and economic stability. In the UK, borrowing costs have climbed to levels not seen since the financial crisis, as markets demand higher returns to compensate for perceived risks.

This creates a more complex picture than it first appears.

While bonds may offer income today, their value can fall when interest rates rise further. At the same time, inflation can erode the real return those yields provide. In other words, a higher headline yield does not automatically mean a better outcome in real terms.

There is also a broader dynamic at play. Governments rely on bond markets to finance spending, which means market sentiment can influence policy decisions, taxation, and even economic direction. Periods of rising yields often reflect underlying stress rather than strength.

This is where caution becomes important.

Moving away from gold into bonds may feel logical in the current environment, but it is not without risk. Bond returns depend heavily on interest rates, inflation, and confidence in government finances, all of which can shift quickly.

Gold, by contrast, does not rely on income or policy decisions in the same way. While its price can fall in the short term, its role as a store of value is less tied to the direction of interest rates.

For investors, the key is understanding that today’s higher yields are part of a changing economic backdrop, not a simple upgrade in opportunity.

XAU/USD Source: Oliver Market Intelligence

A Different Way of Thinking About Money

The key shift is simple but important.

Instead of asking, “How much money do I have?”, a more useful question is, “What can my money buy?”

This perspective focuses on purchasing power rather than headline figures. It also highlights why a rising balance does not necessarily mean rising wealth.

The real question is not only how many pounds you hold, but what those pounds still represent.

If you are considering owning physical precious metals, including gold, silver, platinum or palladium, you can explore your options through www.goldwise.com — where the focus is on ownership, security and transparency.

We are continuing to build Goldwise with content that helps investors understand what is really happening beneath the surface. If there are specific topics you would like us to break down further, or areas you feel are not being covered clearly enough, let us know.

This content is provided for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any investment. The value of precious metals can fall as well as rise, and you may get back less than you invest. Past performance is not a reliable indicator of future results. You should conduct your own research and, where appropriate, seek advice from a qualified financial adviser.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}