Why investors may be underestimating the balance sheet transition unfolding beneath the world economy.

A shipping insurer in London once refused to cover a cargo fleet headed for South America in the late 1940s.

Not because the ships were unsafe.

Not because the goods lacked demand.

But because Britain itself was running out of money.

The empire that had financed global trade for more than a century suddenly depended on foreign creditors, ration books, and dollar loans to maintain stability. Sterling still looked powerful on the surface. London was still London. But underneath, the balance sheet had changed.

And when the balance sheet changes, power eventually follows.

That is the part markets often miss.

Economic dominance rarely disappears overnight. It erodes slowly through debt accumulation, external deficits, and declining productive capacity, long before headlines acknowledge the transition. The shift usually begins quietly inside bond markets, reserve flows, and national accounts before it becomes visible in geopolitics.

Today, something similar may be happening again.

The global conversation still revolves around GDP growth, inflation prints, and central bank meetings. But beneath the noise, a deeper divide is emerging between East and West. One side has spent decades financing consumption through debt expansion and external borrowing. The other has spent decades building reserves, industrial capacity, and creditor positions.

This is no longer just a story about economics.

It is a story about national balance sheets.

The Balance Sheets Behind the Headlines

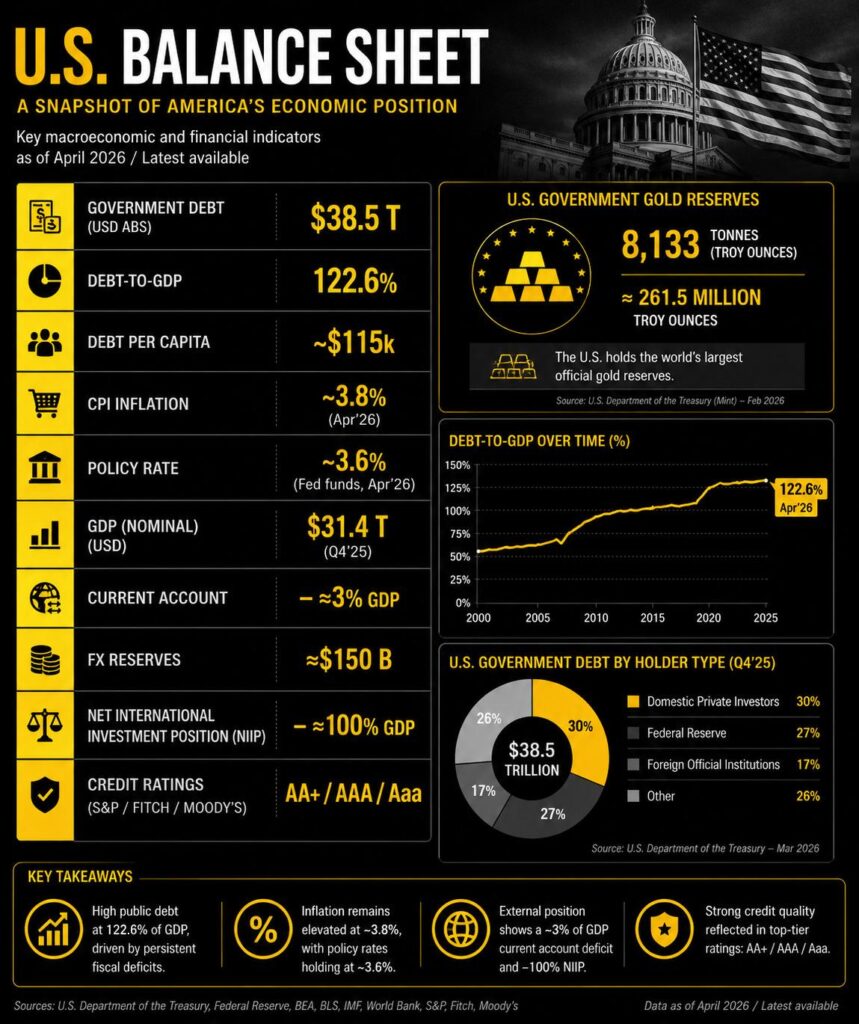

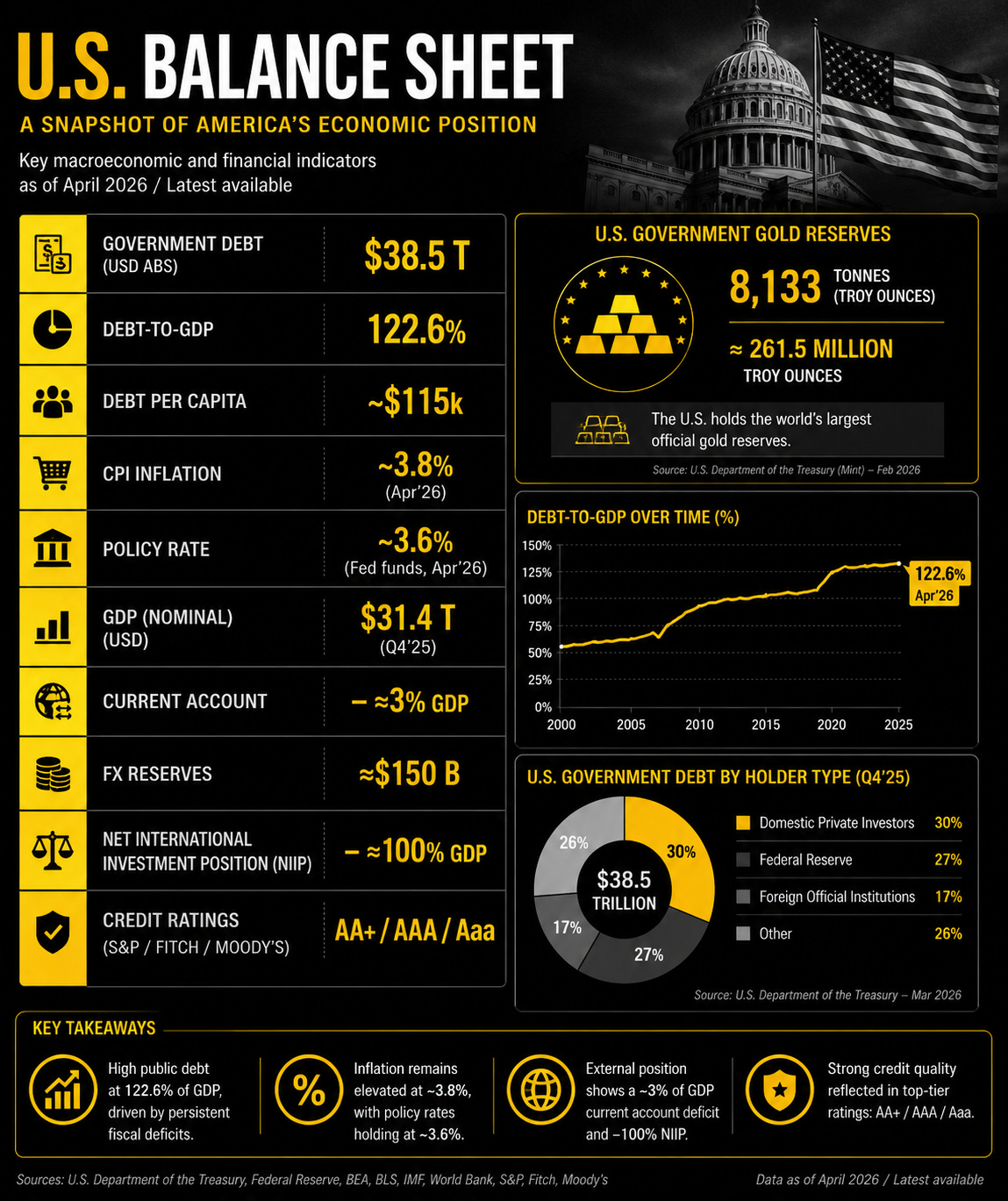

On the surface, the United States still looks unchallenged.

The economy is enormous at more than $31 trillion. The dollar remains the global reserve currency. US equity markets continue attracting foreign capital at an extraordinary scale.

But underneath that strength sits a federal debt load of roughly $38.5 trillion, equivalent to more than 122% of GDP. That translates to approximately $115,000 of federal debt per citizen.

The UK carries debt approaching 94% of GDP, while much of Europe remains heavily leveraged after years of slow growth, ageing demographics, and post-crisis fiscal expansion.

Meanwhile, both the US and UK run persistent current account deficits. In simple terms, they consume more than they produce and rely on external capital to close the gap.

That distinction matters.

Because current account deficits are not merely accounting entries. They represent a transfer of claims. Over time, deficit nations accumulate liabilities while surplus nations accumulate assets.

The West still owns enormous pools of wealth, deep capital markets, and globally dominant financial institutions. But increasingly, its economic model depends on borrowing, financial engineering, and asset inflation to sustain growth.

The East has taken a different path.

China built its rise through manufacturing expansion, export surpluses, and reserve accumulation. Russia, despite sanctions and isolation, maintains relatively low sovereign debt alongside substantial commodity leverage. India, while still developing, carries far lower debt per capita than most Western economies and retains stronger demographic momentum.

The contrast is becoming difficult to ignore.

The Western Model: Growth Through Leverage

The United States: The Reserve Currency Advantage

On the surface, the United States still looks financially untouchable.

The economy remains the largest in the world at more than $31 trillion. The dollar still anchors global trade, sovereign reserves, and international finance. US equity markets continue attracting global capital flows even during periods of political dysfunction and fiscal deterioration.

But beneath that strength sits a debt burden that would have once seemed unimaginable.

Federal debt has now climbed to roughly $38.5 trillion, or more than 122% of GDP. That translates to approximately $115,000 per American citizen. Even more striking, the US continues running large fiscal deficits during periods of relatively full employment, something historically associated with wars or recessions rather than expansionary cycles.

At the same time, America runs a persistent current account deficit, meaning the country consumes more than it produces and relies on foreign capital to fund the gap.

For decades, the system worked because global demand for dollar assets remained insatiable. Foreign governments, institutions, and investors recycled trade surpluses back into US Treasuries and financial markets. The dollar’s reserve currency status effectively allowed the US to borrow more cheaply and more consistently than any nation in modern history.

But there are signs the model is becoming increasingly dependent on leverage rather than productivity.

Debt is growing faster than productive output. Interest costs are consuming a larger share of government revenues. And while the US still dominates technologically and financially, much of its industrial base has steadily migrated abroad over the past three decades.

The US remains the centre of the global financial system.

The question is whether financial dominance alone can indefinitely offset balance sheet deterioration.

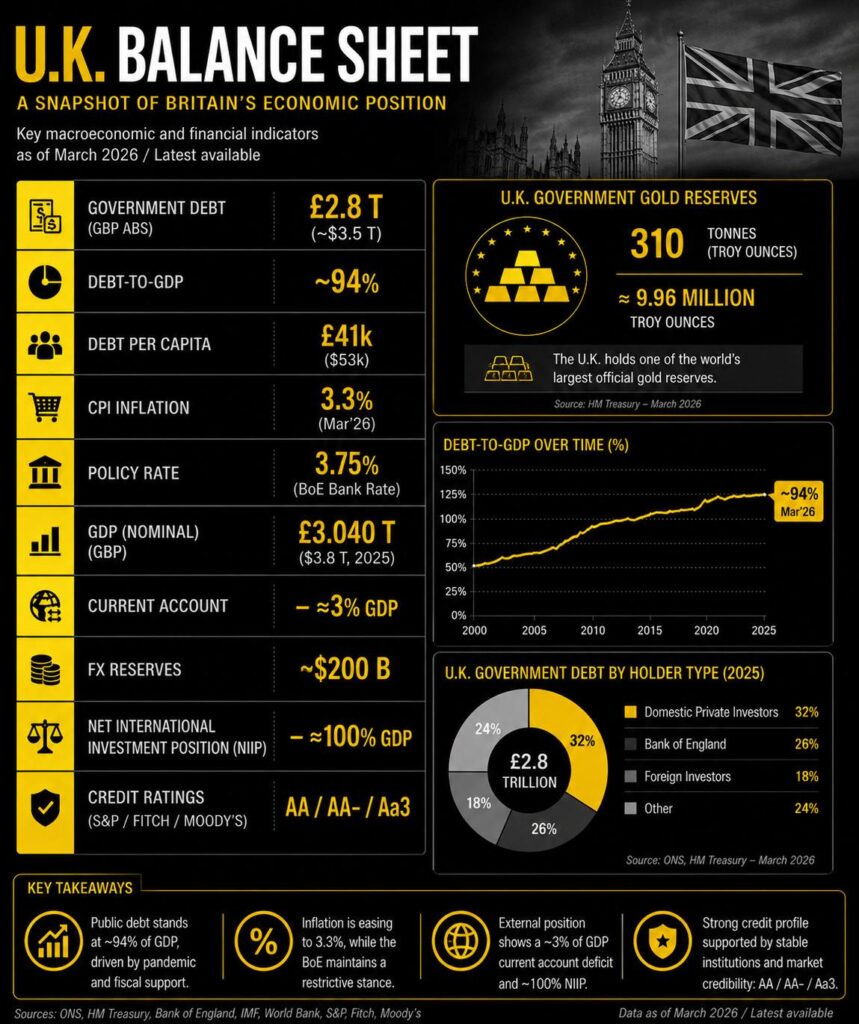

The United Kingdom: From Imperial Creditor to Structural Debtor

Britain’s story is perhaps the clearest historical warning.

A century ago, the UK stood at the centre of global finance, shipping, trade, and reserve currency dominance. Sterling was trusted globally. British capital financed infrastructure projects across continents. London was the unquestioned financial capital of the world.

Today, Britain still retains immense institutional strengths, deep capital markets, and one of the world’s most important financial centres.

But the underlying balance sheet tells a different story.

UK public debt now sits near 94% of GDP, equivalent to around £41,000 per citizen. Economic growth has remained sluggish for years, productivity growth has stagnated, and real wage growth has struggled to meaningfully recover after repeated inflation shocks.

The UK also runs persistent current account deficits, meaning Britain increasingly relies on external financing to support domestic consumption and asset prices.

In many ways, modern Britain reflects the later stages of financialisation.

The economy remains highly sophisticated, but increasingly concentrated around services, finance, housing, and consumption rather than industrial production. Asset values have remained elevated, yet underlying productive growth has weakened.

That does not mean Britain is collapsing.

Far from it.

But it does illustrate how great powers often evolve from production-driven economies into finance-driven economies over time. And historically, that transition tends to coincide with rising leverage and declining geopolitical influence.

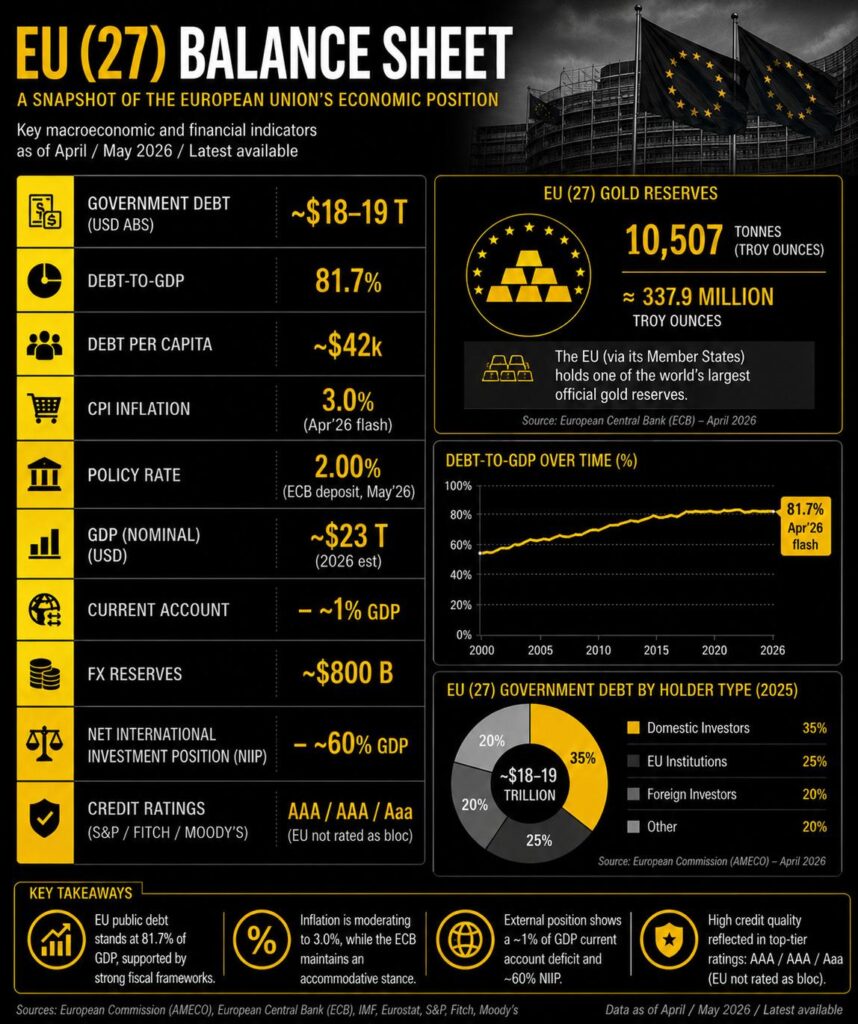

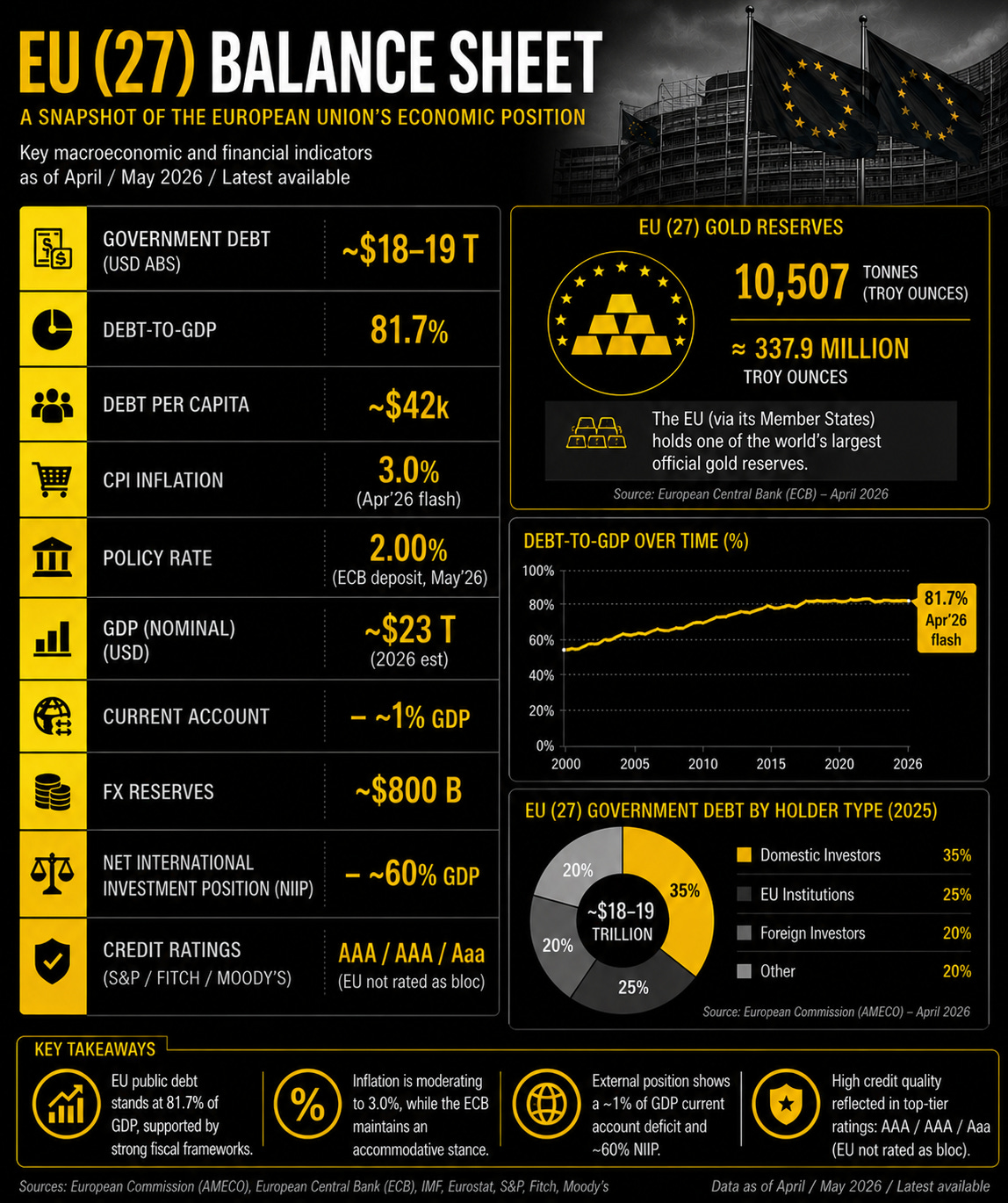

Europe: Wealthy, Stable, and Structurally Slower

Europe presents a slightly different picture.

Unlike the US or UK, the European Union collectively retains stronger trade dynamics and, in some regions, a more substantial industrial base. Germany, in particular, spent decades benefiting from export surpluses and manufacturing competitiveness.

But Europe faces another challenge entirely.

Demographics.

An ageing population, slower productivity growth, rising welfare obligations, and fragmented fiscal coordination have all contributed to structurally weaker growth across much of the continent.

Public debt across the EU now averages more than 80% of GDP, while growth remains subdued despite years of ultra-low interest rates and extraordinary monetary intervention by the European Central Bank.

Europe’s economic model also relied heavily on globalisation.

Cheap Russian energy, Chinese manufacturing demand, and access to global trade flows supported the continent’s industrial machine for decades. But geopolitical fragmentation is now forcing Europe to rethink energy security, supply chains, defence spending, and industrial strategy simultaneously.

That transition is expensive.

And importantly, Europe increasingly finds itself squeezed between two competing superpowers: American financial dominance and Chinese industrial scale.

The result is a region that remains wealthy and institutionally stable, but strategically vulnerable in a more fragmented global order.

The Eastern Model: Production, Reserves, and Strategic Capacity

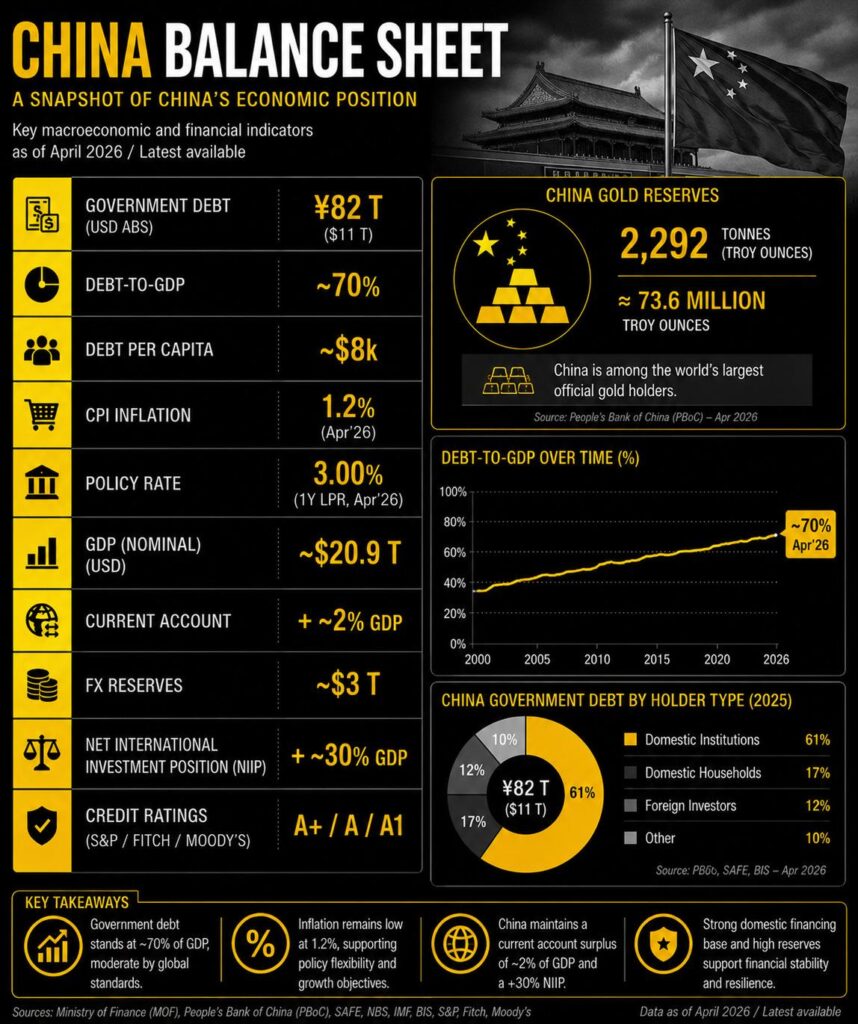

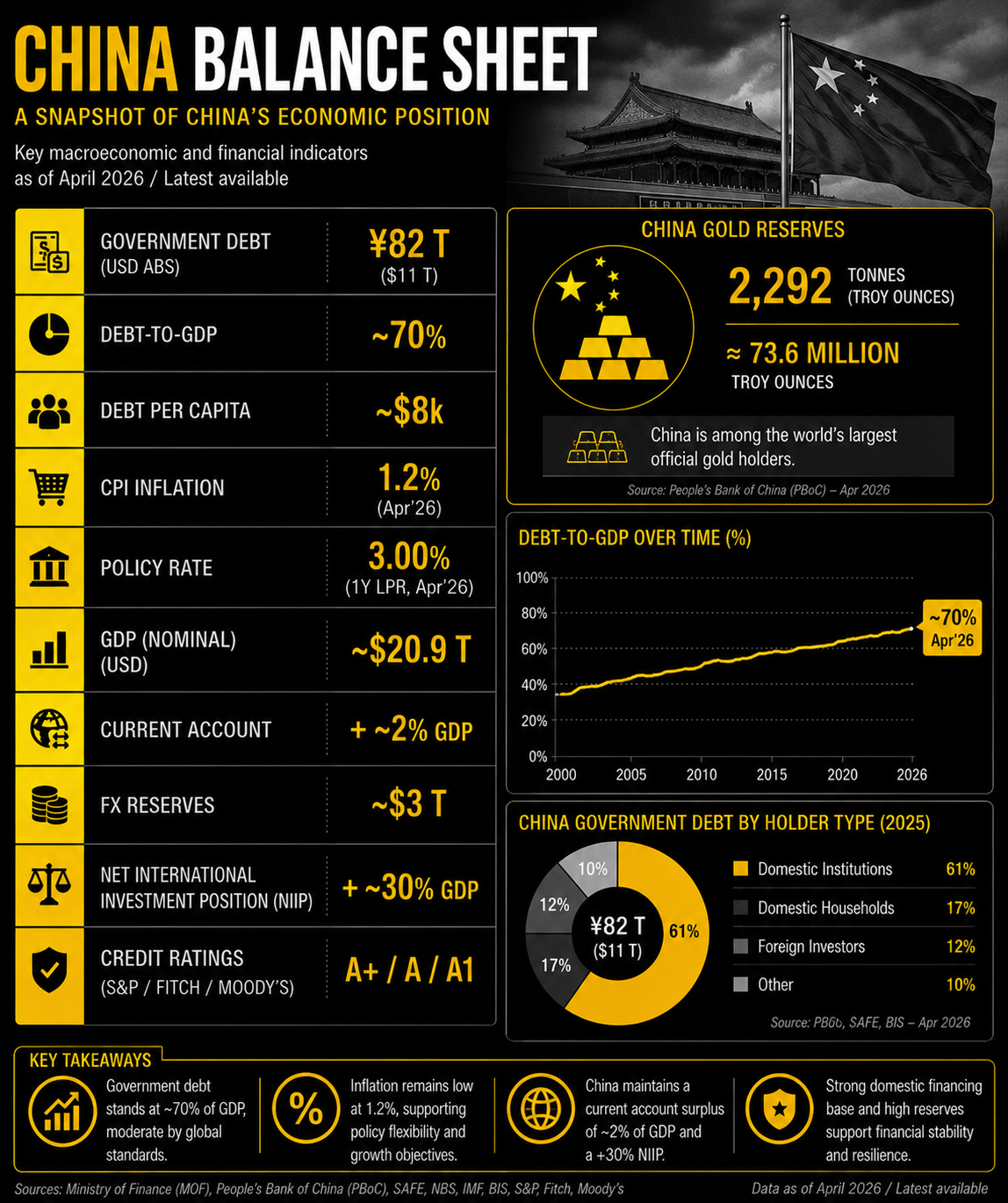

China: The Factory That Became a System

China’s rise is one of the defining economic stories of the modern era.

Over just a few decades, China transformed from a low-cost manufacturing economy into a technological and industrial superpower with influence across supply chains, commodities, infrastructure, and global trade.

Unlike the Western model, China’s growth strategy centred around production first.

High domestic savings, industrial policy, export expansion, and infrastructure investment allowed Beijing to build massive productive capacity while simultaneously accumulating roughly $3 trillion in foreign exchange reserves.

That matters because reserves provide flexibility.

While Western economies increasingly relied on external borrowing and asset inflation, China accumulated claims on the rest of the world through trade surpluses and manufacturing dominance.

Today, China still maintains significantly lower public debt per capita than Western peers, despite concerns around local government liabilities and the property sector.

Its inflation rate also remains relatively subdued at around 1.2%, allowing policymakers far greater room to manage economic slowdowns without triggering the same inflationary pressures facing many Western economies.

But China’s transition is entering a more difficult phase.

The old property-and-infrastructure growth model is slowing. Demographic decline is beginning to emerge. And global resistance to Chinese industrial dominance is rising rapidly, particularly across Europe and the United States.

Still, China retains one enormous advantage.

It continues building real productive capacity at an extraordinary scale.

Whether in electric vehicles, solar technology, batteries, shipbuilding, or advanced manufacturing, China is increasingly shaping the industrial foundations of the next global cycle.

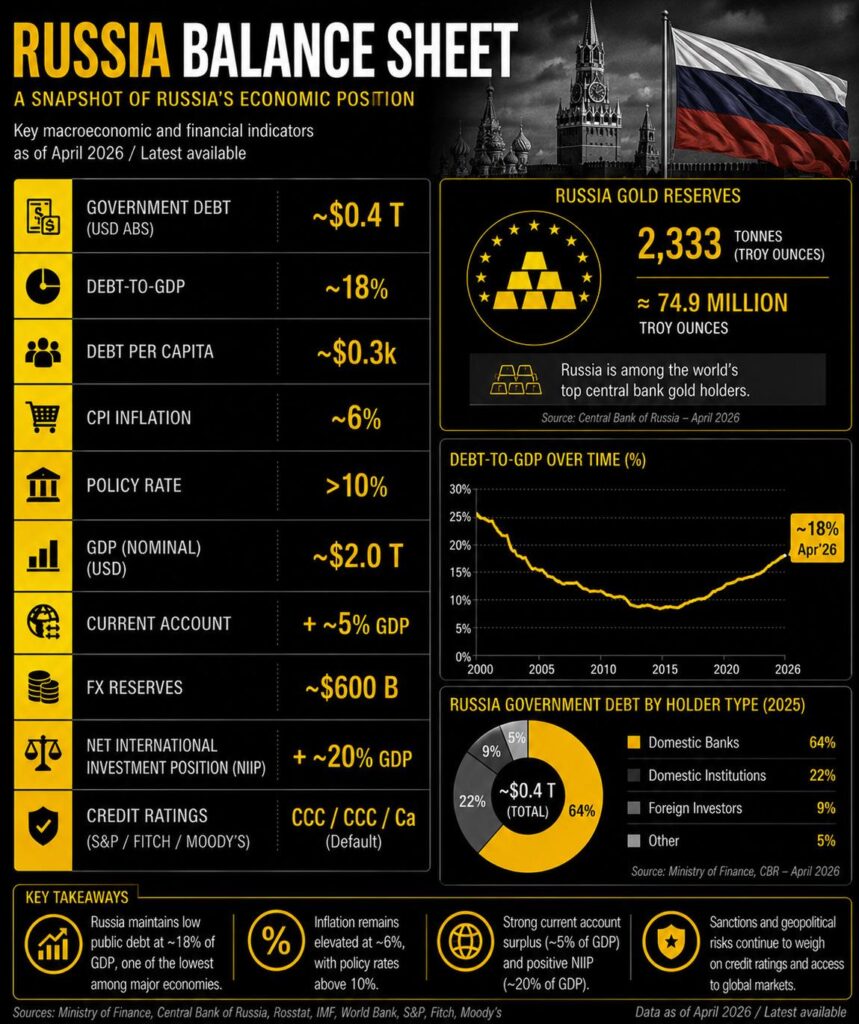

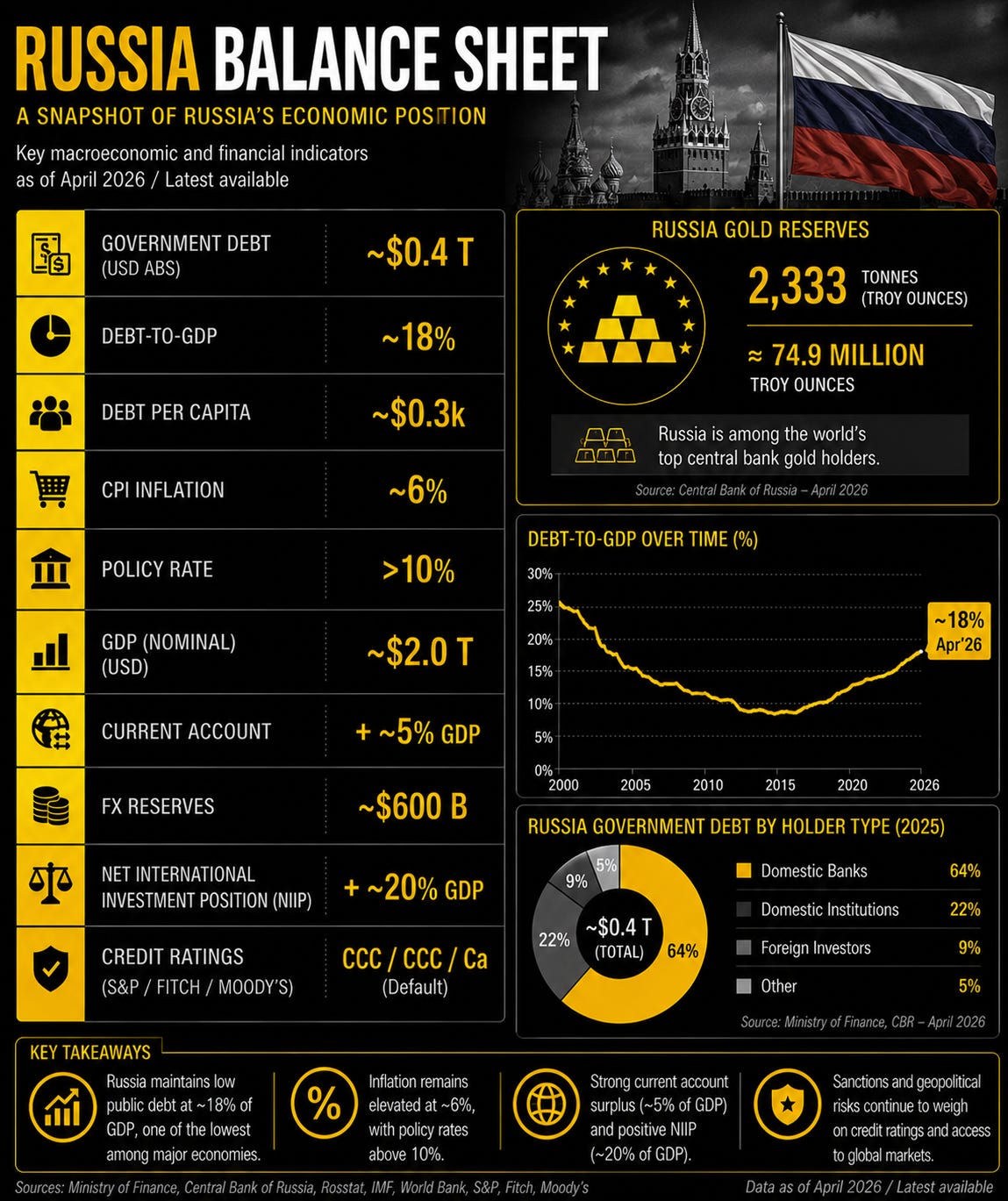

Russia: Resource Wealth and Financial Isolation

Russia occupies a unique position within the global system.

Economically, it is far smaller than both China and the collective West. Yet from a sovereign balance sheet perspective, Russia remains surprisingly conservative.

Government debt sits near just 18% of GDP, among the lowest levels of any major economy. The country also continues running large current account surpluses due to energy and commodity exports.

That surplus matters.

Commodity exporters accumulate external claims during periods of elevated resource prices, allowing them to build reserves and reduce dependency on foreign financing.

Russia’s balance sheet therefore looks very different from highly leveraged Western economies.

But there is a trade-off.

The country faces persistently high inflation, elevated borrowing costs, sanctions pressure, and restricted access to Western financial systems. Capital investment remains constrained and long-term growth prospects are uncertain.

In effect, Russia exchanged integration for resilience.

Its sovereign liabilities remain manageable, but at the cost of isolation from much of the global financial architecture.

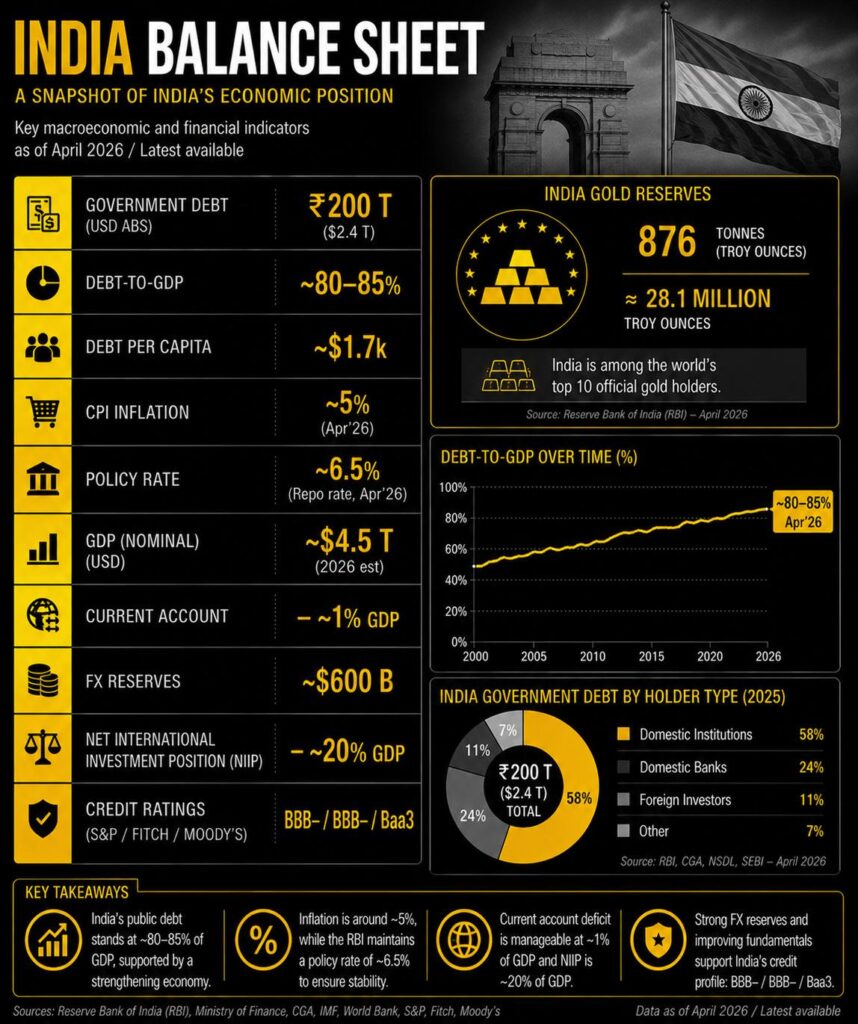

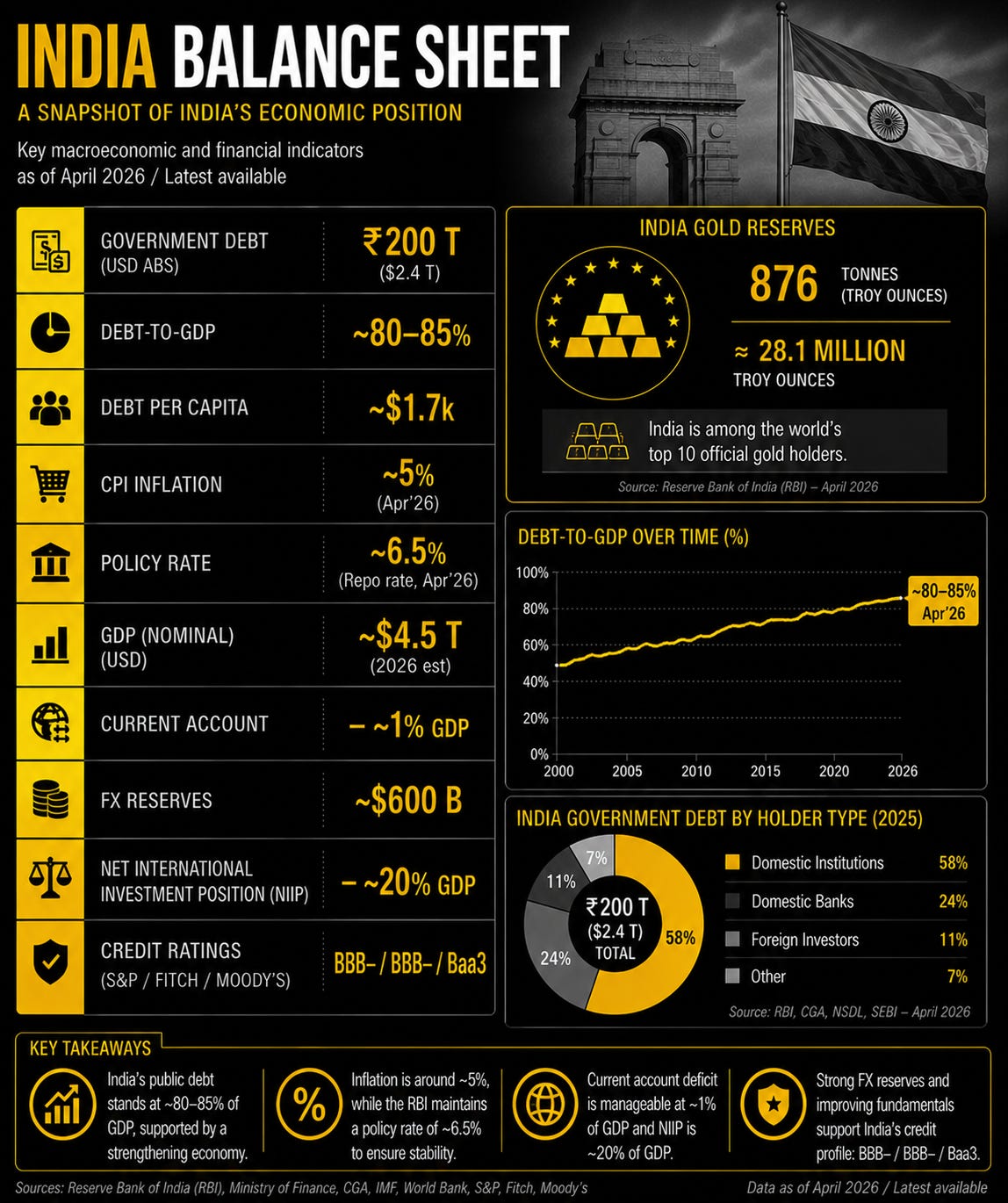

India: The Demographic Counterweight

India may ultimately become the most important long-term story in the Eastern bloc.

Unlike China, India still benefits from favourable demographics, a growing workforce, and rising domestic consumption. While infrastructure and development challenges remain significant, India possesses something increasingly scarce in the developed world: population growth combined with expanding economic capacity.

Public debt levels remain elevated relative to GDP, but debt per capita is still dramatically lower than in the US or UK at roughly $1,700 per person.

That distinction matters because debt burdens ultimately become social burdens.

India also sits in a strategically advantageous position within the emerging geopolitical order. Western firms seeking to diversify supply chains away from China increasingly view India as a critical alternative manufacturing hub.

At the same time, India has carefully balanced relationships between East and West, maintaining ties with Russia while deepening strategic cooperation with the United States and Europe.

India is not yet a financial superpower.

But structurally, it may possess some of the strongest long-term fundamentals of any major economy entering the 2030s.

What Markets May Already Understand Before Policymakers Do

Most investors still focus on the wrong variable.

They watch inflation prints, central bank meetings, and quarterly GDP numbers while missing the structural shift underneath.

This is not simply about growth rates anymore.

It is about who owns assets and who owes liabilities.

The United States still benefits enormously from dollar dominance. Global trade, commodity pricing, and financial markets continue revolving around dollar liquidity. That privilege allows Washington to sustain deficits that most nations could never finance.

But reserve currency status is not permanent law.

Britain once held the same advantage.

At its peak, sterling dominated global trade and finance. London was the centre of the world economy. British debt appeared manageable because global capital trusted the system.

Then the balance sheet deteriorated.

War spending exploded. Industrial competitiveness weakened. External liabilities accumulated. Eventually, the pound lost its dominant position to the dollar.

These transitions take decades.

But they usually begin long before the political narrative catches up.

Today, the US net international investment position sits deeply negative, approaching levels near 100% of GDP. In practical terms, foreign ownership claims on American assets continue rising relative to US ownership abroad.

China and several surplus economies sit on the opposite side of that equation.

That does not guarantee Eastern dominance.

But it does mean the global system is becoming increasingly multipolar financially, industrially, and strategically.

How Great Powers Transition From Assets to Liabilities

This pattern has appeared repeatedly throughout history.

First comes industrial dominance.

Then financial expansion.

Then debt acceleration.

Then external dependency.

The Dutch experienced it.

The British experienced it.

Now parts of the Western system may be entering the later stages of the same sequence.

Meanwhile, rising powers typically begin the cycle with production advantages, stronger savings dynamics, reserve accumulation, and industrial competitiveness.

That does not make them immune from crisis. It simply changes where the vulnerabilities sit.

The United States remains the world’s most powerful financial system. But increasingly, China dominates segments of industrial production that are becoming strategically critical to the next economic era, from electric vehicles to batteries, solar infrastructure, and advanced manufacturing supply chains.

The shift is not clean or linear.

It is messy, political, and deeply interconnected.

Which is precisely why markets are struggling to price it properly.

The Emerging Collision Between Debt and Productive Power

The risk is not simply higher debt levels, it is declining confidence in how those debts are financed and sustained.

The market may also be underestimating how aggressively nations are repositioning around this new balance sheet reality. Trade wars, industrial policy, supply chain reshoring, reserve diversification, and commodity competition are all downstream effects of the same structural transition.

This is why gold continues attracting long-term demand despite higher rates.

Why nations are accumulating strategic commodities.

Why industrial policy has returned globally after decades of financial globalisation.

Countries are beginning to think less like consumers and more like balance sheets again.

And in that environment, productive capacity matters.

Energy matters.

Reserves matter.

Manufacturing matters.

External surpluses matter.

The world is slowly rediscovering the difference between financial wealth and real economic power.

This is not just a story about debt.

It is a story about where economic gravity is moving.

The question is not whether the West collapses or the East rises.

History is rarely that simple.

The question is what happens when a system built on expanding liabilities collides with a world increasingly focused on assets, production, and strategic control.

Because once markets begin pricing balance sheets instead of narratives, the adjustment can happen far faster than most expect.

If you are considering owning physical precious metals, including gold, silver, platinum or palladium, you can explore your options through www.goldwise.com — where the focus is on ownership, security and transparency.

We are continuing to build Goldwise with content that helps investors understand what is really happening beneath the surface. If there are specific topics you would like us to break down further, or areas you feel are not being covered clearly enough, let us know.

This content is provided for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any investment. The value of precious metals can fall as well as rise, and you may get back less than you invest. Past performance is not a reliable indicator of future results. You should conduct your own research and, where appropriate, seek advice from a qualified financial adviser.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}