Kevin Warsh inherits an economy built on assumptions the bond market no longer believes.

In 1979, when Paul Volcker arrived at the Federal Reserve, traders carried calculators the size of bricks and inflation expectations had already seeped into everyday life like cigarette smoke in a crowded bar. Americans rushed to buy appliances before prices rose again. Wage negotiations assumed inflation would continue climbing forever. Bond investors no longer trusted the dollar to preserve value over time.

Volcker’s solution was brutal. He raised rates until parts of the economy snapped under the pressure. Farmers protested outside the Fed. Homebuilders mailed him two-by-fours in anger. Unemployment surged. Yet the market eventually believed him because he demonstrated something rare in modern politics: a willingness to tolerate pain.

Kevin Warsh walks into a different version of the same room. The numbers are cleaner. The language is softer. But beneath the surface, the system feels strangely familiar. Inflation has returned. Treasury yields are climbing. Fiscal deficits are expanding during supposed periods of economic strength. And trust, the invisible scaffolding underneath every fiat system, has started to fray at the edges.

The Vote That Exposed a Fractured America

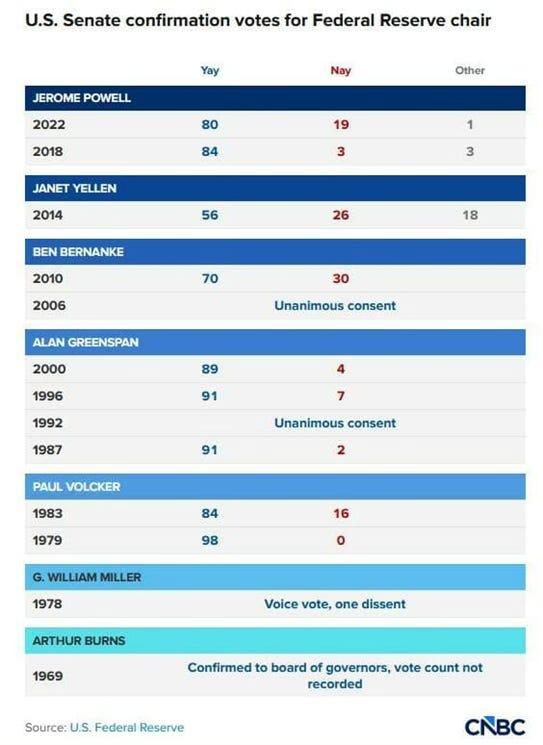

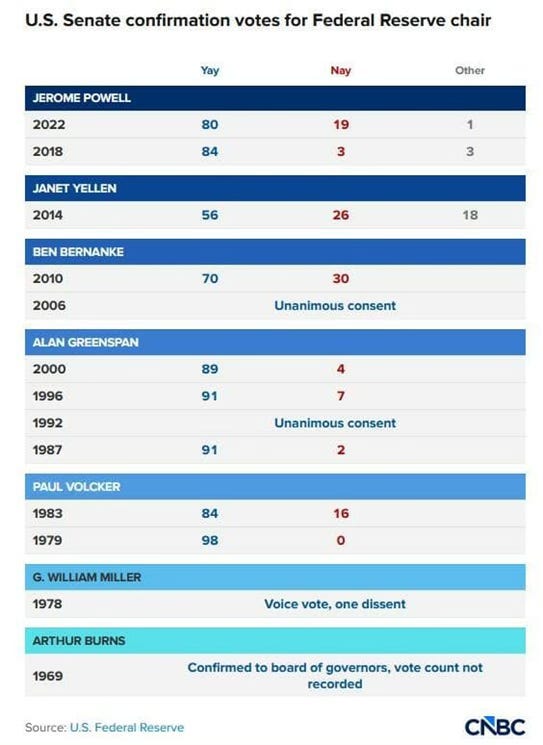

Warsh was confirmed in the closest Senate vote ever for a Federal Reserve chair. Fifty-one to forty-five. Powell sailed through with bipartisan support. Volcker was confirmed almost unanimously. The contrast matters because central banking depends partly on institutional mystique. The Fed works best when markets believe it exists above politics. That illusion now looks difficult to maintain.

Warsh understands the symbolism of the moment. He has spent years arguing that inflation is not some mysterious atmospheric condition that appears spontaneously. His position is far more uncomfortable for Washington. Inflation, in his view, is a policy choice. Excessive government spending paired with perpetual monetary accommodation eventually leaks into prices, asset markets, wages, and expectations.

The argument overlaps heavily with the Fiscal Theory of the Price Level, the increasingly influential idea that inflation is ultimately driven by fiscal credibility rather than simply monetary mechanics.

That distinction quietly changes where blame resides.

Under the old framework, the Federal Reserve could present itself as the technician managing the economy through adjustments in interest rates and liquidity. Under Warsh’s framework, the Fed becomes partially trapped by fiscal behavior it cannot control. The central bank can tighten policy. It can drain reserves. It can slow credit creation. But if Washington continues issuing debt at industrial scale while markets begin doubting repayment through honest money, inflationary pressure eventually re-emerges elsewhere.

That is the trap now tightening around the United States.

Source: U.S Federal Reserve

The Anti-QE Chairman

Warsh’s instincts are, in many ways, anti-Bernanke. He despises quantitative easing outside emergency conditions. He resigned from the Fed in 2011 partly in protest against QE2, later describing the policy as a reverse Robin Hood operation that inflated asset prices while widening inequality. He views the Fed’s bloated balance sheet as economically distorting and politically corrosive.

In theory, this sounds refreshing after fifteen years of monetary excess. Markets addicted to central bank liquidity have increasingly behaved like spoiled children who panic whenever stimulus is removed. The Fed became less a lender of last resort than a permanent market backstop.

The problem is that systems built on cheap debt rarely tolerate detoxification gracefully.

Warsh appears to believe a productivity boom driven by artificial intelligence can create enough disinflationary pressure to allow lower short-term rates without reigniting inflation. It is a seductive idea. If AI dramatically boosts productivity, goods and services become cheaper to produce, margins improve, and inflation naturally softens. This would allow the Fed to lower rates while simultaneously shrinking its balance sheet.

That is the optimistic version.

The Bond Market Has Started Voting

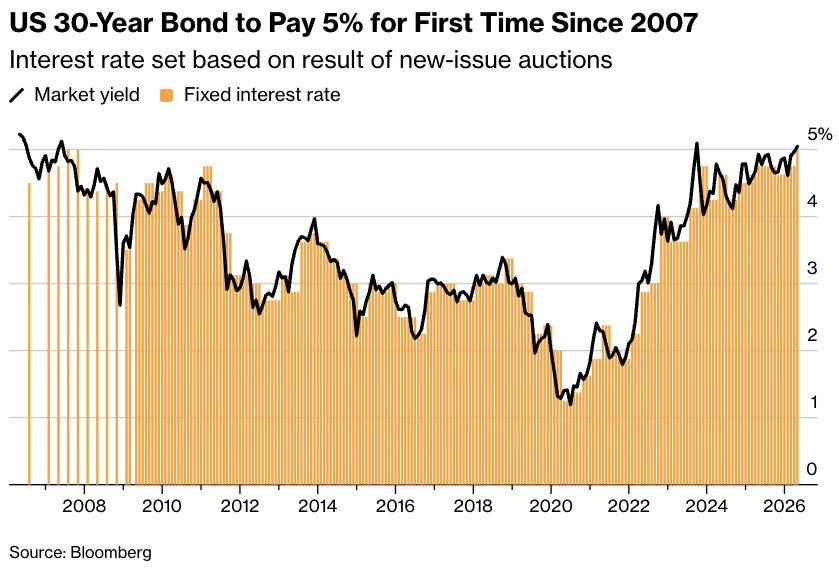

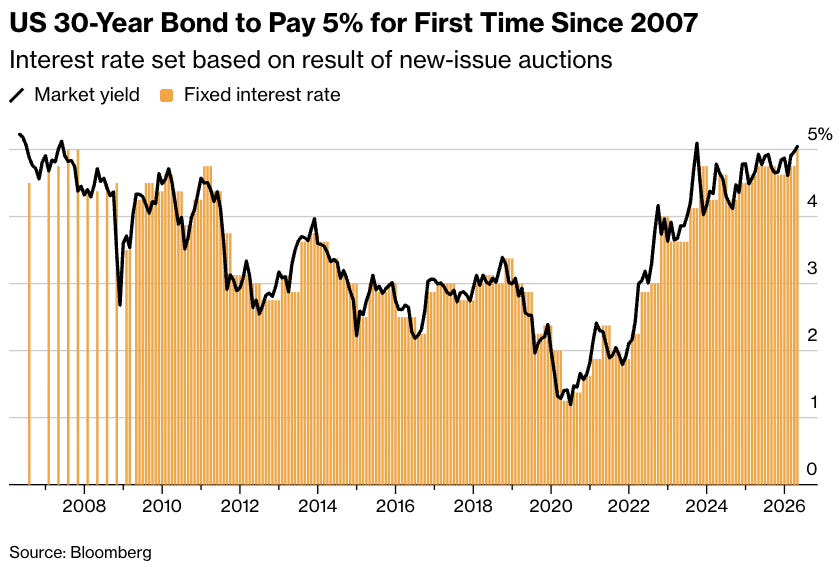

The darker reality is sitting in the Treasury market.

Thirty-year Treasury yields pushing above 5% are not just another market headline. They represent something more psychologically dangerous: lenders demanding compensation for long-term uncertainty surrounding inflation, deficits, and fiscal credibility. Once bond markets begin questioning whether future dollars will retain purchasing power, the entire architecture of modern finance starts wobbling.

This is why Warsh may discover very quickly that the Federal Reserve chair is no longer the dominant actor in the system.

The debt itself is becoming the protagonist.

America now carries debt levels that effectively require some combination of financial repression, currency debasement, inflation, or default-by-devaluation to remain manageable over time. Politicians rarely say this directly because voters still imagine debt as something eventually repaid honestly. Historically, heavily indebted states tend to resolve the problem differently. They dilute the currency quietly while maintaining the appearance of nominal repayment.

The mechanism changes. The destination rarely does.

Warsh can shrink the Fed’s balance sheet. He can alter inflation metrics, as he hinted by favoring Trimmed Mean PCE over core PCE. He can attempt to engineer lower short-term rates while allowing longer yields to absorb fiscal pressure. But he cannot eliminate the arithmetic underneath the structure.

Source: Bloomberg

The Debt Clock Nobody Can Stop

The federal government now spends extraordinary amounts simply servicing existing debt. Higher yields accelerate the problem. Every refinancing cycle becomes more expensive. Every Treasury auction matters more. At some point, the market starts asking uncomfortable questions about sustainability.

And once trust weakens, policymakers lose optionality frighteningly fast.

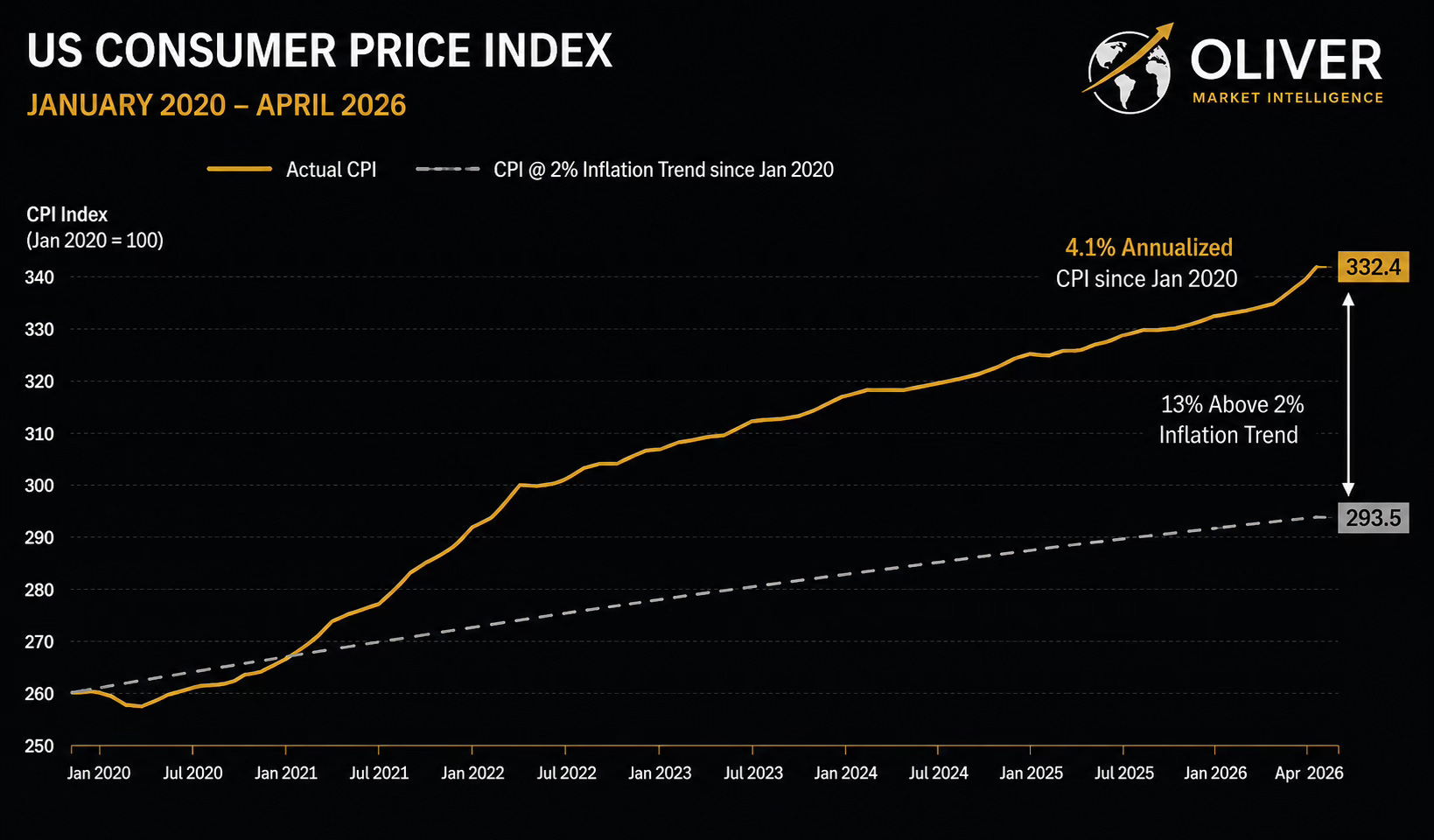

This is where gold enters the conversation again, not as a speculative trade or apocalyptic fetish object, but as a monetary asset rediscovering its historical role.

For decades, bonds functioned as the world’s reserve collateral because they represented safety, liquidity, and predictable real returns. That assumption is deteriorating. Real yields swing violently. Sovereign debt issuance expands endlessly. Central banks intervene constantly. Bonds increasingly behave like political instruments rather than neutral stores of value.

Gold does not carry counterparty risk. It does not require confidence in a finance ministry, a treasury secretary, or a central bank chairman. It simply exists outside the promises.

That distinction becomes more valuable as promises multiply faster than productive output.

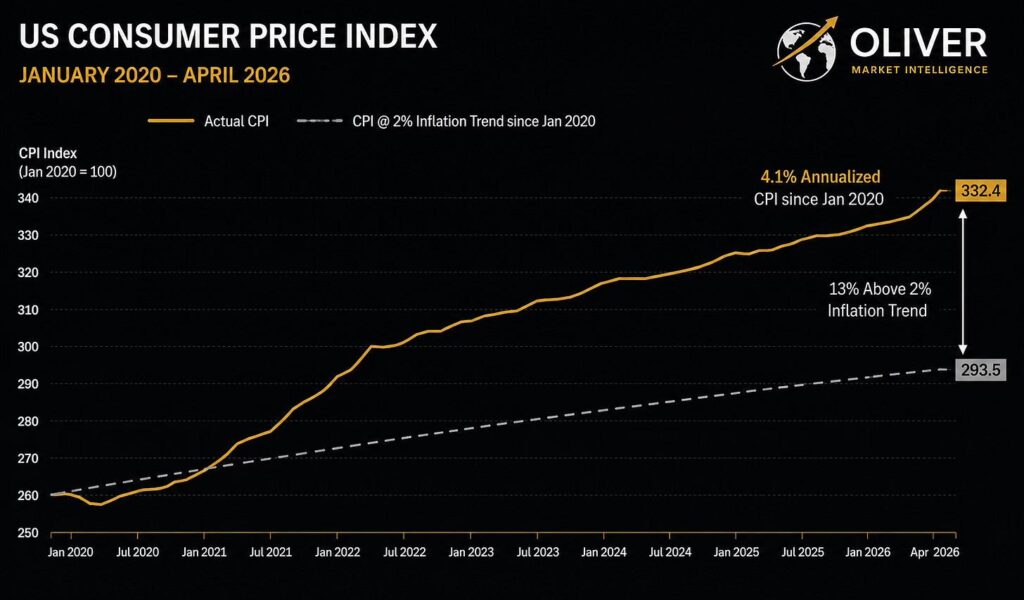

Source: Oliver Market Intelligence

Why Gold Is Quietly Replacing Bonds

Critics often point out that gold produces no yield. That criticism made more sense in an era where bonds reliably protected purchasing power. Today many sovereign bonds offer negative real returns once inflation is honestly measured. Investors are slowly rediscovering that preserving capital and compounding capital are no longer the same exercise.

The irony surrounding Warsh is difficult to ignore. He may genuinely understand many of the system’s underlying problems better than his predecessors. He appears more intellectually honest about the distortions created by endless QE. He recognises that inflation emerges from political incentives, not just temporary supply shocks. He understands the corrosive social consequences of asset inflation.

Yet understanding the disease does not guarantee the ability to cure it.

The modern financial system has become structurally dependent on debt expansion. Markets require liquidity. Governments require refinancing. Consumers require cheap credit. Asset prices require accommodative conditions. Even modest tightening now causes visible fractures somewhere in the system, whether commercial real estate, regional banks, sovereign debt markets, or consumer credit.

The Fed still controls interest rates at the short end of the curve. But the bond market increasingly controls credibility.

That is a very different balance of power than the one Volcker inherited decades ago.

The Fed Cannot Print Trust

Back then, the system still possessed enough productive strength and demographic momentum to absorb severe tightening. Today the structure feels older, heavier, more fragile. Like a casino running smoothly only as long as nobody tries cashing out simultaneously.

Which brings us back to that smoky room in 1979.

Volcker walked in with the authority to impose pain because the public still believed pain could restore stability. Warsh inherits a country where voters demand low inflation, rising asset prices, cheap mortgages, expanding government benefits, strong employment, and lower interest rates all at once. Financial markets demand the same contradiction.

That is not monetary policy. That is political fantasy.

And fantasies tend to end the same way: slowly at first, then all at once.

If you are considering owning physical precious metals, including gold, silver, platinum or palladium, you can explore your options through www.goldwise.com — where the focus is on ownership, security and transparency.

We are continuing to build Goldwise with content that helps investors understand what is really happening beneath the surface. If there are specific topics you would like us to break down further, or areas you feel are not being covered clearly enough, let us know.

This content is provided for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any investment. The value of precious metals can fall as well as rise, and you may get back less than you invest. Past performance is not a reliable indicator of future results. You should conduct your own research and, where appropriate, seek advice from a qualified financial adviser.

{kind=link}

{kind=link}

{kind=link}

{kind=link}